8 Survival analysis in HTA

8.1 Introduction

Survival modelling is a cornerstone of biostatistical analysis, specifically designed to model time-to-event outcomes, such as the overall time between the beginning of an observation or exposure (e.g. diagnosis of cancer) until a relevant event (typically death, or progression to a different health state). This represents a powerful analytic framework that provides much more granular information than cruder binary (event vs no-event) analyses, thus enabling the estimation of richer output, including instantaneous and cumulative risks, over time.

In typical biostatistics applications, survival modelling is used to understand the magnitude of treatment effects and identify prognostic factors, accounting for the data-generating mechanism. In the context of HTA, it also plays a pivotal role, because decisions are made at the population level and often require extrapolation beyond the follow-up observed in clinical studies. Accurate survival estimates are therefore essential not only for quantifying treatment effectiveness but also for projecting downstream costs, quality-adjusted life years and overall cost-effectiveness.

Whenever possible, modelling at the individual-level allows the incorporation of patient heterogeneity, adjusting for covariates and the propagation of uncertainty that can then inform robust evidence-based policy decisions. This makes survival analysis both a statistical and an economic tool, bridging clinical evidence with the long-term evaluations required for health system decision-making.

While the overall methodology is well established, its application in HTA does have some specific quirks, which are deeply related to the nature of the available data, as well as the fundamental focus on decision-making, rather than simple inference. For these reasons, which we explore in details below, survival methods applied in HTA are often “non-standard”, in comparison to those used in “biostatistical” modelling. Despite the underlying complexity, survival analysis is extremely prevalent in HTA, because it is the natural modelling framework for cancer studies, which represent a large proportion of all the HTA appraisals (Latimer, 2011).

In this chapter, we provide a general framework for survival analysis, specifically for HTA and focus on a number of “typical” distributional assumptions, as well as on computational methods that are particularly efficient for this type of outcome. Jackson et al. (2025) provide a wider introduction (with larger focus on non-Bayesian modelling), while aspects of HTA modelling related to survival analysis are also presented in Dias et al. (2018, chap. 10) and in Sharples and Demiris (2020).

NoteNotation for survival modelling

As suggested in Note 4.1 in Section 4.2, throughout this chapter we slightly modify our general notation, in which we have used the symbol \(t\) to index the treatments under consideration.

In order to align with the general survival analysis literature (and because, hopefully, there is no major confusion with the rest of the book), in this chapter, we indicate with \(t_i\) the main outcome of the analysis, i.e. the time until a relevant event happens for individual \(i\).

We also use throughout this chapter the index \(k=1,\ldots,K\) to indicate relevant parts of the models, as in Equation 8.8, or in Equation 8.13.

8.2 General framework for survival analysis

The general modelling framework for time-to-event, can be described as follows. The main outcome is the observed time at which the event under study is recorded for the \(i-\)th individual, \(t_i\). We can describe the sampling variability in the observed times using a density \(f(t_i\mid \boldsymbol\theta)\), as a function of a set of relevant parameters.

In addition, we can consider a number of helpful quantities to describe the survival mechanism: the first and, perhaps, most important is the survival function \[ S(t\mid\boldsymbol\theta) = \Pr(T>t) = 1-F(t\mid\boldsymbol\theta) = 1 - \int_0^t f(u\mid\boldsymbol\theta)du, \] where \(F(t\mid\boldsymbol\theta)\) is the cumulative density of the variable \(T\). The survival function describes the probability of an individual surviving beyond time \(t\).

Other important quantities are the hazard function \[ h(t\mid\boldsymbol\theta) = \lim_{dt \rightarrow 0}\frac{\Pr(t\leq T < t+dt \mid T\geq t)}{dt}, \tag{8.1}\] which quantifies the instantaneous risk of experiencing the event, as well as the related cumulative hazard function \[ H(t\mid\boldsymbol\theta)=\int_0^t h(u\mid\boldsymbol\theta) du. \]

NoteBrothers and sisters

By their mathematical properties, we can retrieve a set of useful relationships that allow us to connect \(F(\cdot)\), \(S(\cdot)\). \(f(\cdot)\), \(h(\cdot)\) and \(H(\cdot)\). Thus, specifying one of them is sufficient to fully characterise the survival model.

By definition, the density function is the derivative of the cumulative function, with respect to the time variable \[\displaystyle f(t\mid\boldsymbol\theta)=\frac{d}{dt}F(t\mid\boldsymbol\theta)=F^\prime(t\mid\boldsymbol\theta). \tag{8.2}\]

As the numerator of Equation 8.1 is a conditional probability, it can be factorised into the ratio of the joint to the marginal probabilities (see Section 5.2.2) and thus \[ \begin{aligned} h(t\mid\boldsymbol\theta) & = \lim_{dt \rightarrow 0}\frac{\Pr(t\leq T < t+dt,T\geq t)}{\Pr(T\geq t)dt} = \lim_{dt \rightarrow 0}\frac{\Pr(t\leq T < t+dt)}{S(t\mid\boldsymbol\theta)dt} \\ & = \frac{f(t\mid\boldsymbol\theta)dt}{S(t\mid\boldsymbol\theta)dt} = \frac{f(t\mid\boldsymbol\theta)}{S(t\mid\boldsymbol\theta)}, \end{aligned} \tag{8.3}\] because, obviously, the probability that \(T\) is in the interval \([t; t+dt)\) and, at the same time, \(T\geq t\) is just \(\Pr(t\leq T < t+dt)\); and, by definition, \(f(\cdot)dt\) is the probability that the variable \(T\) is in a small interval of width \(dt\).

Combining the definition of the survival function and Equation 8.2, its derivative with respect to the time variable is the negative of the density function \[\displaystyle S^\prime(t\mid\boldsymbol\theta)=\frac{d}{dt}S(t\mid\boldsymbol\theta)=\frac{d}{dt}\left[1-F(t\mid\boldsymbol\theta)\right]=-f(t\mid\boldsymbol\theta). \tag{8.4}\]

Combining Equations 8.3 and 8.4, the hazard function can be represented as the ratio of the derivative to the actual survival function \[\displaystyle h(t\mid\boldsymbol\theta)=-\frac{S^\prime(t\mid\boldsymbol\theta)}{S(t\mid\boldsymbol\theta)}. \tag{8.5}\]

Given Equations 8.1 and 8.5, as well as the basic properties of differential calculus, the cumulative hazard function can also be expressed also as the negative log-survival \[\displaystyle H(t\mid\boldsymbol\theta)=\int_0^t -\frac{S^\prime(u\mid\boldsymbol\theta)}{S(u\mid\boldsymbol\theta)}du=-\log(S(t\mid\boldsymbol\theta)). \tag{8.6}\]

8.2.1 Censoring

Another important defining feature of time-to-event data is the fact that, almost invariably, the evidence in the observed data is limited. This is because, most often, the length of the follow-up is not enough for us to be able to observe the event under study on all the individuals involved – a phenomenon typically referred to as censoring1.

Thus, in addition to the observed times \(t_i\), we usually consider an event indicator \(d_i\) (for “dummy” variable), taking value 1 if the event actually happens within the time horizon during which the data are observed, or 0 when the \(i-\)th individual is “censored”.

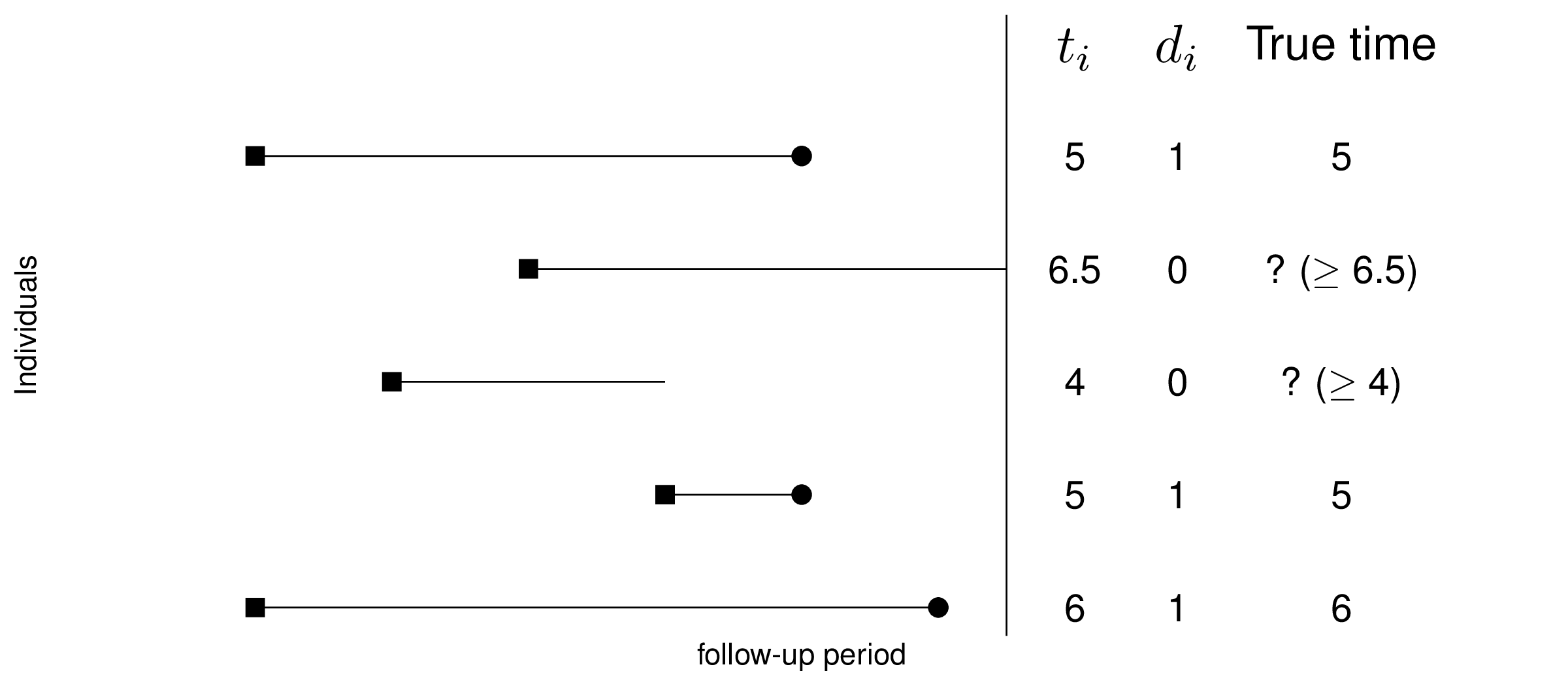

If \(d_i=1\), then \(t_i\) is fully observed; conversely, if \(d_i=0\), we do not know whether the event actually occurs – it may in the future, but we just do not have this information. Consequently, when \(d_i=0\), then the observed \(t_i\) does not represent the true “survival time”. Figure 8.1 depicts this by showing that for some individuals the entire history is known, while for others, key information (e.g. whether the event is actually occurred) is not available.

Censoring is important, because just like missing data (see Chapter 10), it implies that the information present in the data is not complete. Consequently, in the presence of censoring, the individual contribution to the likelihood function is expressed as \[ \mathcal{L}(\boldsymbol\theta\mid t_i,d_i) = h(t_i\mid\boldsymbol\theta)^{d_i} S(t_i\mid\boldsymbol\theta). \tag{8.7}\] Basically, if the individual is not censored (i.e. they have survived up to \(t\) and hence \(d_i=1\)), their risk of experiencing the event is simply described by the full density function, expressed as \(h(t_i\mid\boldsymbol\theta) S(t_i\mid\boldsymbol\theta)\) – see Equation 8.3; if, on the other hand, they are censored (i.e. \(d_i=0\)), then their risk is measured by the survival function as the probability that they will experience it in the future (after time \(t\)).

Equation 8.7 can be used (typically taking the log, for computational stability) to perform calculations on the density \(f(\cdot)\) – we return to this point in Section 8.3.4.

8.3 Survival analysis in HTA

In typical applications of survival analysis, e.g. in the context of randomised clinical trial, the main objective of the statistical analysis is to estimate the impact of a number of covariates (including the treatment arm) on the survival time. This sort of structure is applied specifically for cancer drug trials. In these cases, typically, the analysis is focused on a head-to-head comparison between a new intervention (e.g. a new cancer drug) and some sort of standard of care (e.g. chemotherapy).

In the case of survival modelling in HTA, there are at least two added complications that must be carefully taken into account.

8.3.1 Extrapolation

Almost invariably, the nature of these studies implies a time horizon that does not allow to follow-up all the individuals enrolled until they experience the event of interest (usually, sadly, death), through the effect of censoring and other considerations (e.g. treatment switching for lack of efficacy – see for instance Latimer et al., 2016).

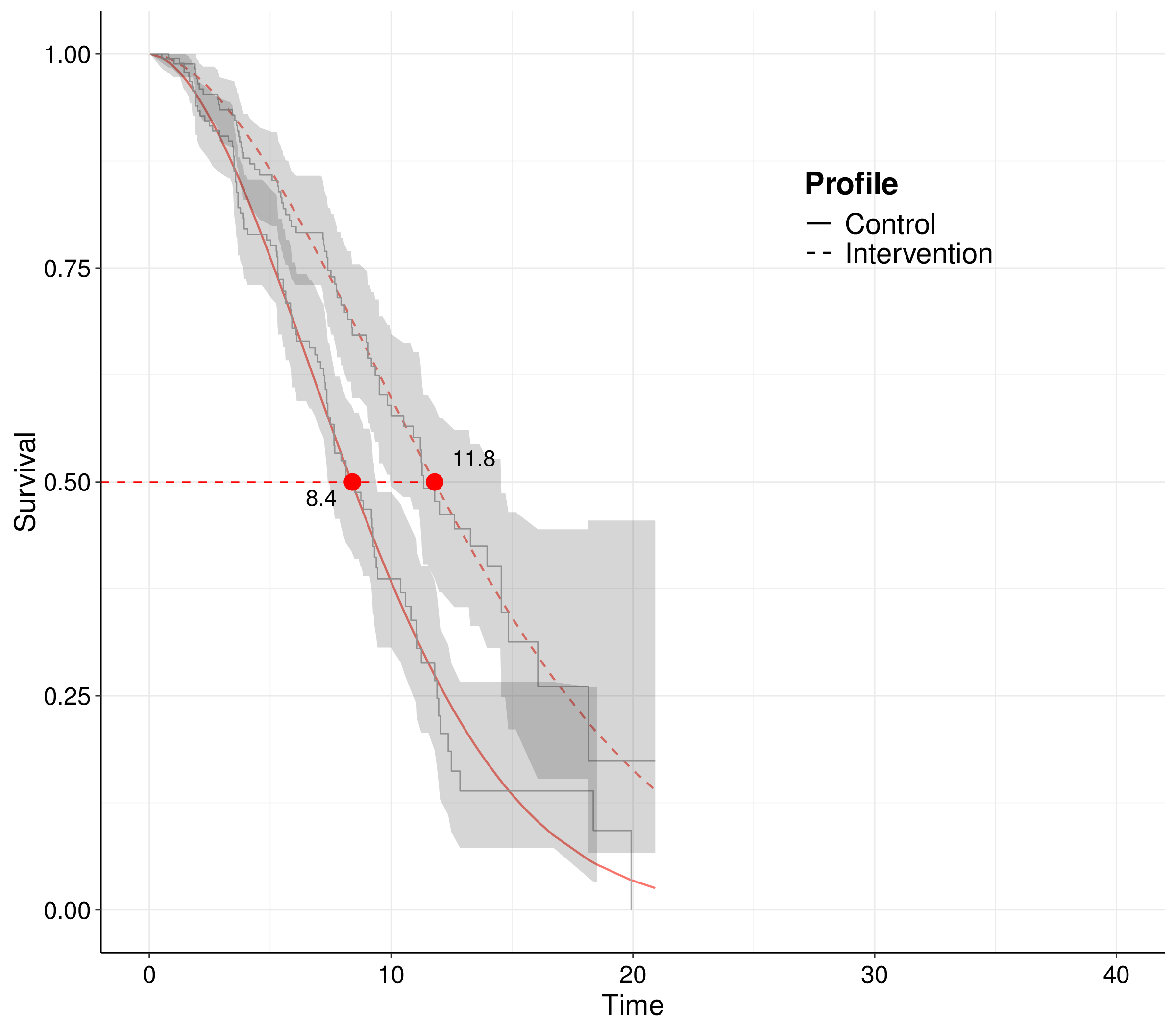

Figure 8.2 (a) shows the typical representation of trial data in the form of Kaplan-Meier (KM) curves (Kaplan and Meier, 1958) – see Note 8.1 below for more technical details. These are non-parametric estimators for the probability of survival at any given time point over the duration of the follow-up in a study and are shown as the step curves (surrounded by a non-parametric 95% interval estimate). KM estimates are ubiquitous in survival analysis, as they are a very efficient way of summarising the observed data.

Alongside the KM curves for the two treatment arms (generically labelled as “Control” and “Intervention”), we have included two smooth curves, fitted to the observed data to estimate survival over the observed study period. The two dots on the smooth curves indicate the estimated median survival time, i.e. the point along the \(x\)–axis in correspondence of the value of 50% along the \(y\)–axis.

In typical survival studies, the median time is one of the quantities of interest because, as shown in Figure 8.2 (a), we do not have enough observations to be able to estimate the survival curves all the way down to 0, i.e. at the point when all the observed individuals actually experience the event. Notice that in the case depicted in Figure 8.2 (a), censoring is actually not too extreme, as indicated by the fact that both curves are reasonably close to 0 (especially for the controls). Nonetheless, for the intervention arm, there is about 15% of individuals for whom we do not know the time at which the event (death) occurs and hence both the KM and the smooth curve end abruptly at the end of the follow-up time.

This is in contrast with the needs of the HTA analysis: we cannot just rely on the difference we measure in the study period, e.g. in this case a treatment effect of 11.8 \(-\) 8.4 = 3.4 units of time, say months, in terms of median survival. That is because the economic analysis must take a “life-time horizon”: if a treatment is approved for reimbursement, it will be provided to individuals for as long as they need it and the effects must then be measured in terms of mean, rather than median survival time.

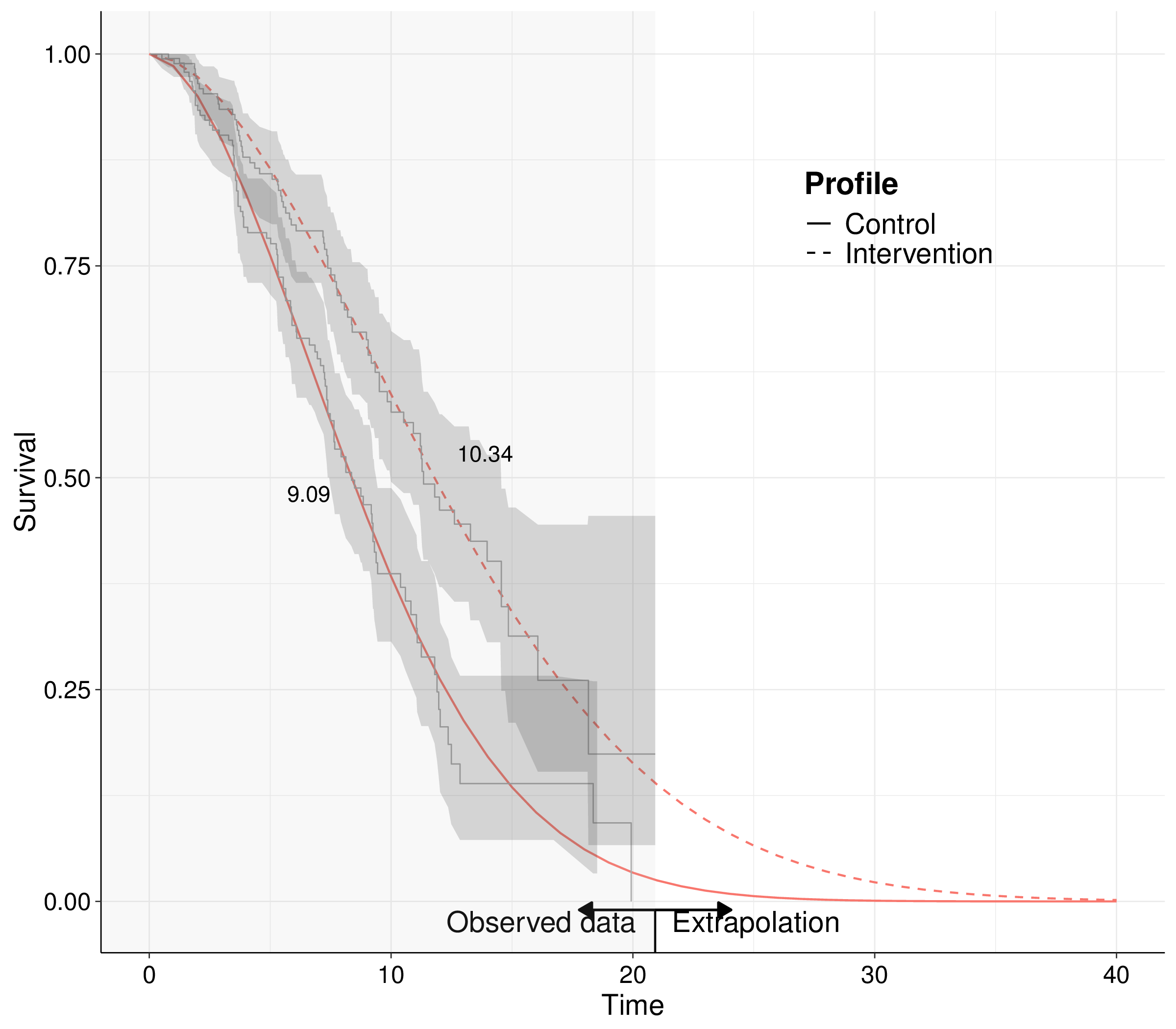

Figure 8.2 (b) shows this by expanding the smooth curve beyond the duration of the observed times – this is typically referred to as extrapolation. By expanding the time horizon to, in this particular case, over 40 units of time, we ensure that the survival curves go down to 0, to the point where all the individuals will have experienced the event under study. This is necessary because, integrating by part and using Equation 8.4, we can prove that the mean survival time is equivalent to the full area under the survival curve: \[ \text{E}[T] := \int_0^\infty t f(t\mid\boldsymbol\theta)dt = \int_0^\infty S(t\mid\boldsymbol\theta) dt. \]

Importantly, if we are able to extrapolate the survival curve over a longer time horizon, the treatment effect may vary even substantially: in the case of Figure 8.2 (b), it is 10.34 \(-\) 9.09 = 1.25 units of time, in terms of mean survival – that is basically half the median treatment effect that we get from the trial data with no extrapolation.

There are two main obvious implications of this issue. Firstly, in HTA it is harder to apply standard modelling for survival analysis, such as Cox Proportional Hazard models (Cox, 1972). This is because, while they have the great advantage of not committing to a fully parametric specification for the time-to-event variable, their semi-parametric nature makes it harder to produce time-quantile predictions, e.g. extrapolate the survival curves.

For this reason, in HTA we tend to rely more heavily on parametric models for survival analysis, which do require more explicit assumptions. Therefore, the way in which we produce this extrapolation beyond the observed trial data becomes crucial and may exert notable sensitivity to the overall economic results (Latimer, 2011).

Note 8.1: Kaplan-Meier estimates

Imagine we have a fictional dataset recording the time-to-event for \(n=10\) individuals, as \(\boldsymbol{t}=( 0.03,0.03,0.92,1.48,1.64,1.64,1.7,1.7,1.74,1.77 )\). The data can be aggregated by listing the unique times at which events happen and counting the progression of individuals from being “at risk” (i.e. exposed to the risk of the event) to having actually experiencing it. Table 8.1 shows this aggregation.

| Time | At risk | Events | Survivors |

|---|---|---|---|

| 0.00 | 10 | 0 | 10 |

| 0.03 | 10 | 2 | 8 |

| 0.92 | 8 | 1 | 7 |

| 1.48 | 7 | 1 | 6 |

| 1.64 | 6 | 2 | 4 |

| 1.70 | 4 | 2 | 2 |

| 1.74 | 2 | 1 | 1 |

| 1.77 | 1 | 1 | 0 |

The KM estimator for the survival curve is formally defined as \[ S^{\text{KM}}(t) = \prod_{i: t_i \leq t} \left(1 - \frac{m_i}{r_i}\right), \] where: \(\mathcal{R}_t = \{i: t_i \leq t\}\) indicates the risk set, i.e. the set of observed times below the index value \(t\); \(m_i\) is the total number of events observed in each of the times in the risk set; and \(r_i\) is the number of individuals at risk in each of the times included in the risk set.

In the example of Table 8.1, the survival curve for the third time (\(t=0.92\)) can be computed as \[ \begin{aligned} S^{\text{KM}}(0.92)& = \left(1-\frac{0}{10}\right)\left(1-\frac{2}{10}\right)\left(1-\frac{1}{8}\right) \\ & = 1 \times \frac{8}{10} \times \frac{7}{8} = \frac{7}{10}. \end{aligned} \] This estimate holds until the next observed unique time – thus, in this case, we would estimate \(S^{\text{KM}}(t)=0.7\) for \(t \in [0.92;1.48)\). This gives KM estimates the typical “step-function” shape displayed in Figure 8.2 (a). Note that censoring is automatically accounted for in this computation, because the denominator is represented by the risk set, which excludes censored individuals.

8.3.2 Digitised data

One further problem with survival modelling in HTA is that, while it may be possible to access individual-level data for a specific study comparing an active (and typically innovative) treatment against some standard of care (placebo, or existing technologies, such as chemotherapy), it is very unlikely that we have available all individual-level data for all the relevant treatments, for which we may only have access to aggregated level data (cfr. Chapter 6).

Interestingly, graphical representations of the data are typically produced in the literature, in the form of Kaplan-Meier estimates, as shown in Figure 8.2 (a). Suitable algorithms exist that are able to process the image depicting the KM curves from a given study and recreate a synthetic dataset that resembles the original one, in the sense that if a KM estimated is produced using the synthetic data, the images would be very close. Zhang et al. (2024) have recently produced an R package (and a corresponding R Shiny web-application) to perform this operation, while other proprietary software, e.g. DigitizeIT or Enguage, is also available for the same purpose.

The use of digitised survival data has become increasingly popular, especially in HTA, because it allows to recreate a set of individual-level datasets that can be used to expand the full survival modelling to all the relevant comparators in an economic evaluation, effectively expanding the analysis of aggregated data. One (but not the only – we return to this point in Section 9.3.2) key limitation of digitised data is that the KM estimates are typically presented conditionally only on the treatment arm, as in Figure 8.2 (a). Every other covariate that may be of interest (e.g. sex, age, comorbidities or cancer stage at diagnosis) is averaged out in the KM curves that can be digitised. Nonetheless, this form of synthetic information is very often the only one available to modeller and thus it can be helpful, if used wisely.

In addition (and perhaps even more importantly), landmark trials upon which the evaluation of the time-to-event is based report outcomes both in terms of overall survival (OS; i.e. the time from enrollment to death) and using a surrogate progression-free survival (PFS, indicating the time from enrollment until “progression” to a worse status of prognosis). While the focus of the economic evaluation is on OS, often data from clinical experimentation are not mature enough to observe many deaths during the course of the follow-up; conversely, progression data tend to have lower amount of censoring and thus are often used as a proxy for OS – see also Green et al. (2025), who develop a model based on a Bayesian hierarchical structure similar to those discussed in Chapter 6, to “borrow” strength from the more mature PSF curves and estimate OS with increased precision.

In the case of digitised data, because the curves are presented separately, in the absence of further information, it is impossible to embed the underlying correlation in the two outcomes. In other words, in the actual dataset, there may be individuals who first progress and then die and these will contribute to both the PFS and OS curves. However, simple digitisation process will not allow us to determine who they are and effectively only generate two separate, independent datasets: one with synthetic data on the time to progression and one with synthetic data on the time to death.

Using suitable algorithms (such as the one described in Guyot et al., 2012), it is possible to correctly estimate the number of individuals at risk at different points on a time-grid, thus properly accounting for censoring. Nonetheless, the overall limitation of using digitised over fully individual-level survival data remains.

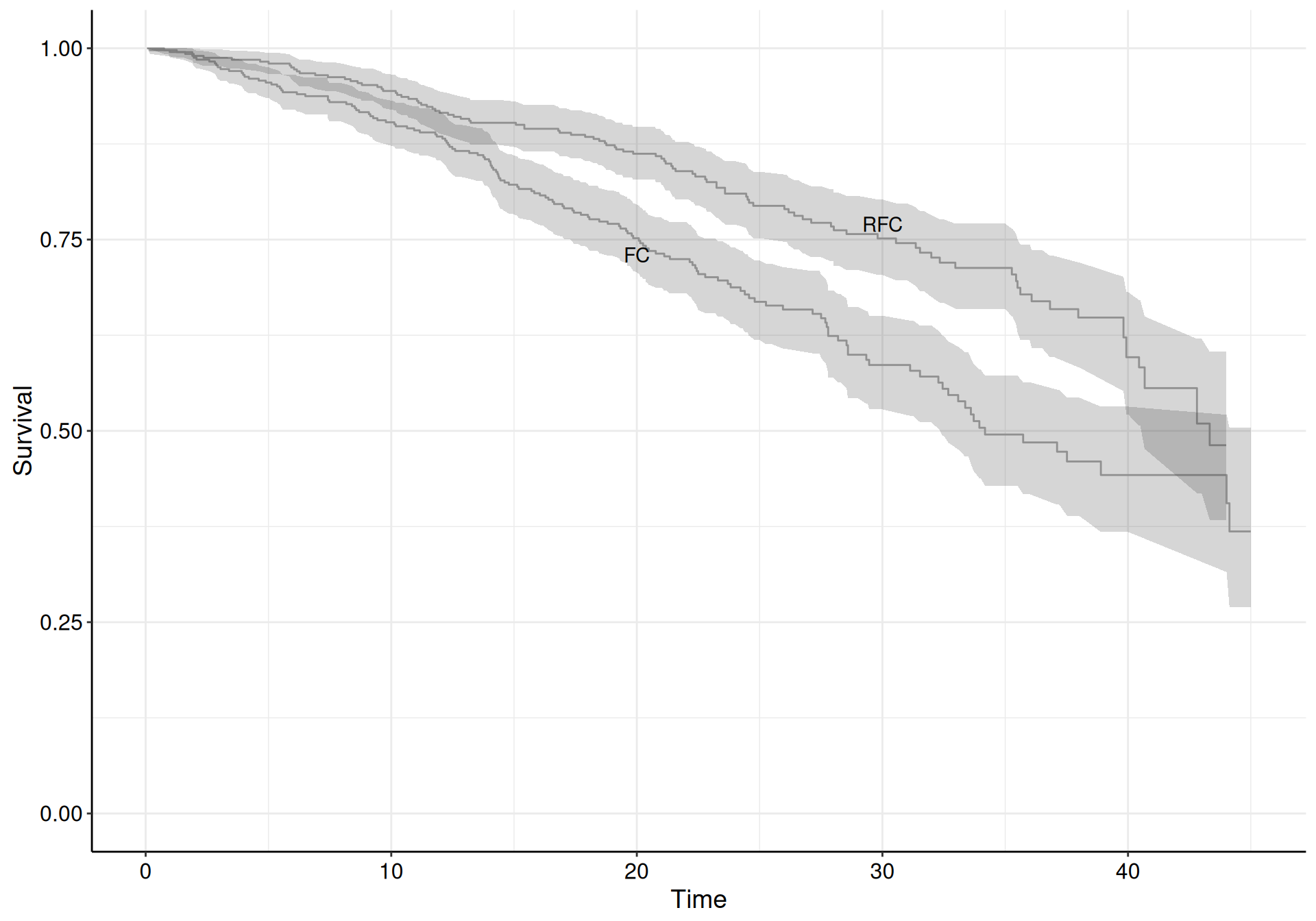

Example 8.1. NICE Technical Appraisal 174 (adapted from Williams et al., 2017). We focus here as a running example on one of NICE’s technical appraisals (TAs), specifically TA174 (NICE, 2009). This considers a full economic evaluation of rituximab in combination with fludarabine and cyclophosphamide (RFC) against fludarabine and cyclophosphamide alone (FC) for the first-line treatment of chronic lymphocytic leukemia (CLL-8).

Although the original data used in NICE (2009), mainly based on Hallek et al. (2010), are not publicly accessible, in their tutorial on using R to model survival analysis for economic evaluation, Williams et al. (2017) make available a digitised version of the dataset, which we use as our motivating example. This version of the original dataset is also included in the R package survHE (Baio, 2020) – see Section 8.4.

Note 8.2: Digitising well is hard work…

The data presented by Williams et al. (2017) benefit from a further layer of substantive post-processing, which allowed the research team to reconstruct (a very good approximation of) the full trajectory of each individual patients.

First, the KM curves for OS, PFS and Post-Progression Survival (PPS), available from Hallek et al. (2010) have been digitised, accounting for censoring, so that there were as many times points as there were patients.

Secondly, an iterative process was performed, to keep calculating KM estimates with the generated data, until all the event and censored times were reconstructed “in the right place”, i.e. so that they matched the survival probabilities from the curves at each time to within an arbitrary margin of error of 0.005, in most cases.

The event times from the PFS and OS curves that most closely matched were assumed to be deaths without progression. This left the other PFS events as progressions and the other OS events as deaths after progression. This process is fairly straightforward in this particular study, because there are not too many deaths. The progression and death time for each individual were finally recreated by matching a progression time from the PFS curve with a time from the PPS curve that gave a death after progression time from the OS curve.

Obviously, this procedure does not retrieve the original data for all the individual trajectories with absolute certainty and therefore the digitised and post-processed dataset is merely an approximation to the “truth”.

| ID | Progression? | Death? | Progression time | Death time | Treatment |

|---|---|---|---|---|---|

| 1 | 1 | 0 | 31.991 | 32 | RFC |

| 2 | 1 | 0 | 30.552 | 30.6 | RFC |

| 3 | 1 | 0 | 27.906 | 28 | RFC |

| 4 | 1 | 0 | 2.877 | 3 | FC |

| 5 | 1 | 0 | 0.978 | 1.11 | FC |

| 6 | 1 | 0 | 1.611 | 1.77 | FC |

The data contain much information – for each individual (labelled in the ID column, in Table 8.2), we observe a treatment indicator, along two further indicators for whether progression and/or death have been observed (1) or not (0). The time (in months) at which these occur is also recorded – if either progression or death do not occur, the time is the point at which the individual is censored, i.e. they exit the observation. Because of the approximation in the digitisation and post-processing, there are some (relatively minor) discrepancies with the original data: for instance, Hallek et al. (2010) report 106 progressions in the RFC arm, while the synthetic data only count 104.

In the rest of this chapter, we consider a version of the overall dataset (which we, creatively, name data), which focuses on progression. In other words, if an individual either dies or is not observed to progress within the follow-up of the study, they are considered as censored (and the variable status is set to 0 – see Example 9.5 for more details on how to retrieve this dataset).

Figure 8.3 shows the KM curves for the two treatment arms. In the beginning and at the end of the follow-up period, there does not seem to be much separation among the two curves, when we also consider the interval estimates. In the middle of the observation period, however, the RFC arm seem to have better survival, as the KM curve is higher.

Table 8.3 shows the estimated numbers behind the KM curves. We report here, for simplicity, the first and last three times at which the estimates are produced, for both the treatment arms. In each row, we include the number of observed events (individuals who have a progression within the period defined by the two consecutive times), the overall number of individual at risk and the number of individuals censored, in that period.

| RFC | FC | ||||||

|---|---|---|---|---|---|---|---|

| Time | Events | At risk | Censored | Time | Events | At risk | Censored |

| 0.058 | 0 | 407 | 1 | 0.058 | 0 | 403 | 1 |

| 0.748 | 1 | 406 | 0 | 0.173 | 1 | 402 | 0 |

| 0.806 | 0 | 405 | 1 | 1.266 | 1 | 401 | 0 |

| \(\ldots\) | \(\ldots\) | \(\ldots\) | \(\ldots\) | \(\ldots\) | \(\ldots\) | \(\ldots\) | \(\ldots\) |

| 44.016 | 1 | 12 | 0 | 43 | 0 | 22 | 4 |

| 44.131 | 1 | 11 | 0 | 43.326 | 1 | 18 | 0 |

| 45 | 0 | 10 | 10 | 44 | 0 | 17 | 17 |

8.3.3 Modelling

Generally speaking, assuming the data include a vector of covariates \(\boldsymbol{x}\), (e.g. age, sex, comorbidities, clinical history, trial arm, etc.), we can describe the vector of relevant parameters as \(\boldsymbol\theta=\left(\mu(\boldsymbol{x}),\alpha(\boldsymbol{x})\right)\), where \(\mu(\boldsymbol{x})\) is a location parameter, which indicates the mean or the scale of the probability distribution used to model the sampling variability in the time-to-event data, described by the density \(f(t\mid \boldsymbol\theta)\). As for \(\alpha(\boldsymbol{x})\), this is a (set of) ancillary parameters, characterising the shape or variance of the underlying distribution.

Even though we may assume that the observed covariates modulate both the location and the ancillary parameters, most often, we simply limit the dependence for \(\mu(\boldsymbol{x})\) and model \(\alpha\) independently on \(\boldsymbol{x}\) – Latimer (2011) suggests ways in which we can still incorporate the dependence on the covariates in shape parameters too (see Section 8.4.5 for more discussion).

Notice also that in a parametric formulation such as this, the main quantities of interest, \(S(t\mid\boldsymbol\theta)\) and \(h(t\mid\boldsymbol\theta)\) can be written down as functions of \(\left(\mu(\boldsymbol{x}),\alpha(\boldsymbol{x})\right)\) and thus, once we can produce suitable estimates for them, we can simply plug in any value for \(t\) in that functional form to extrapolate the survival or hazard.

We typically use a generalised linear formulation \[ g(\mu_i) = \eta_i = \beta_0 + \sum_{k=1}^K \beta_k x_{ik} [+ \ldots] \tag{8.8}\] Here, the function \(g(\cdot)\) is usually the logarithm – and, in line with Baio (2020), we slightly abuse the notation and omit the dependence of \(\mu_i\) on \(\boldsymbol{x}\), for simplicity. As discussed in Section 5.2, the notation \([+ \ldots]\) indicates that Equation 8.8 can be extended to additional terms, e.g. random effects to account for repeated measurements or clustering. This may be relevant, for instance, in the case of multi-site trials, or for “tumour-agnostic” experimentation, in which the same treatment is used across different cancer types, if they share the same underlying molecular abnormality.

Table 8.4 presents some selected choices to model the sampling variability for the observed and censored times, as well as the mathematical expression for the resulting density, the relationship linking the location parameter \(\mu_i\) to the linear predictor \(\eta_i\), as defined in Equation 8.8 and the functional form of the survival function, depending on the model parameters \(\boldsymbol\theta=(\mu_i,\alpha)\). More detailed accounts for parametric survival models are presented, for example, in Latimer (2011), Cox (2008), or Jackson et al. (2025).

| Distribution | Density $f(t_i\mid\mu_i,\alpha)$ | Location $\mu_i$ | Survival $S(t_i\mid\mu_i,\alpha)$ |

|---|---|---|---|

| Exponential | \(\displaystyle \mu_i \exp\left(-\mu_i t_i\right)\) | \(\displaystyle \exp(\eta_i)\) | \(\displaystyle \exp\left( -\mu_i t_i \right)\) |

| Weibull | \(\displaystyle\frac{\alpha}{\mu_i} \left( \frac{t_i}{\mu_i} \right)^{\alpha-1}\exp\left(- \left(\frac{t_i}{\mu_i}\right)^\alpha\right)\) | \(\displaystyle \exp(\eta_i)\) | \(\displaystyle \exp\left( -\left(\frac{t_i}{\mu_i}\right)^\alpha \right)\) |

| Gamma | \(\displaystyle \frac{\mu_i^\alpha}{\Gamma(\alpha)}t_i ^{\alpha-1}\exp(-\mu_i t_i)\) | \(\displaystyle \exp(\eta_i)\) | \(\displaystyle 1-\frac{1}{\Gamma(\alpha)}\gamma(\alpha,\mu_i t_i)\) |

| Gompertz | \(\displaystyle \mu_i e^{\alpha t_i}\exp\left( -\frac{\mu_i}{\alpha\left(e^{\alpha t_i}-1\right)} \right)\) | \(\displaystyle \exp(\eta_i)\) | \(\displaystyle \exp\left( \frac{-\mu_i}{\alpha(e^{\alpha t_i}-1)} \right)\) |

| log-logistic | \(\displaystyle \frac{(\alpha/\mu_i)(t_i/\mu_i)^{\alpha-1}}{1+(t_i/\mu_i)^\alpha}\) | \(\displaystyle \exp(\eta_i)\) | \(\displaystyle \left(1+\left(\frac{t_i}{\mu_i}\right)^{\alpha}\right)^{-1}\) |

| log-Normal | \(\displaystyle \frac{1}{t_i\alpha\sqrt{2\pi}}\exp\left( -\frac{(\log t_i - \mu_i)^2}{2\alpha^2} \right)\) | \(\displaystyle \eta_i\) | \(\displaystyle 1-\Phi\left( \frac{\log t_i - \mu_i}{\alpha} \right)\) |

Note 8.3: Weibull parameterisations

Table 8.4 shows one specific parameterisation for the Weibull distribution, in terms of a scale \(\mu_i\) and a shape \(\alpha\). This particular parameterisation gives rise to an accelerated failure time (AFT) interpretation, which amounts to assuming that the effect of a covariate is to accelerate or decelerate the life course of a disease by some constant.

To give a general intuition, we may consider the old cliché that every year in a dog’s life is equivalent to about seven human years. Indicating the survival functions for humans and dogs as \(S_H(t\mid\boldsymbol\theta)\) and \(S_D(t\mid\boldsymbol\theta)\) respectively, we can summarise this by assuming that \[ S_D(t\mid\boldsymbol\theta) = S_H(7t\mid\boldsymbol\theta), \] which essentially implies that the chances of a dog surviving past \(t\) years are identical to those of a human surviving past \(7t\) years – in other words, dogs go through life seven times faster than humans.

Generally speaking, in an AFT model, we compare survival across two different “profiles” (e.g. covariates specifications) through an acceleration factor (e.g. the multiplier set at the value 7, in the dogs’ life example). If this acceleration factor is greater than 1, then “exposure” benefits survival, while if it is less than 1, then it is detrimental.

The Weibull distribution also has a different parameterisation, which allows the proportional hazard (PH) interpretation. If we model \[ t\sim\text{Weibull}(\mu^*_i,\alpha) \qquad \mbox{with}\qquad p(t\mid\mu^*_i,\alpha)=\mu^*_i \alpha t_i^{\alpha-1}\exp\left(-\mu^*_i t_i^\alpha\right), \] then we can prove that \(S(t\mid\mu^*_i,\alpha)=\exp\left(-\mu^*_i t_i^\alpha\right)\). Using Equation 8.3, the hazard function is computed as \[ \begin{aligned} h(t\mid\mu^*_i,\alpha) & = \mu^*_i \alpha t_i^{\alpha-1} \\ & = \exp(\eta^*_i) \alpha t_i^{\alpha-1} \\ & = \exp\left(\beta^*_0 + \sum_{k=1}^K \beta^*_k x_{ik}\right) \alpha t_i^{\alpha-1}. \end{aligned} \] This implies that if we compare two profiles differing only in the value of one covariate in the linear predictor by taking the ratio of their respective hazard functions, then all the other terms cancel out and the coefficient of that covariate, \(\beta^*_k\), is the (log-)hazard ratio.

Some simple algebra shows that, interestingly, we can retrieve the PH parameterisation from the AFT one, by setting \[ \mu_i = \exp\left(-\frac{\eta_i}{\alpha}\right) = \exp\left(-\frac{\beta_0 + \sum_{k=1}^K \beta_k x_{ik}}{\alpha}\right). \tag{8.9}\]

We return to this point in Section 8.3.5.

More generally, of the models described in Table 8.4, in the basic format: the Weibull and Exponential have both a PH and AFT interpretation, the Gompertz is PH only and the Gamma, log-Normal and log-logistic are AFT only.

NICE Decision Support Unit document (Latimer, 2011) presents an even larger set of potential distributional assumptions for the density \(f(\cdot)\) than these in Table 8.4; while this was never intended to be prescriptive, but rather to serve as guidance for practitioners, many applications of survival modelling in HTA have taken this literally, with the consequence that, often, practitioners feel like they must test all the models described in the NICE guidance document.

8.3.4 Bayesian modelling

In a Bayesian setting, in addition to identifying a parametric model to describe the sampling variability in the observed (and censored) data, we need to include a suitable prior distribution for the model parameters \(\boldsymbol\theta\). Baio (2020) summarises the main features of the various parametric models mentioned in Latimer (2011), alongside some default minimally vague specification for the prior distributions for the relevant specification of \(\boldsymbol\theta\).

In the context of Equation 8.8, this amounts at least to the set of regression coefficients \(\boldsymbol\beta=(\beta_0,\ldots,\beta_K)\), for which we can typically use a prior of the form \(\boldsymbol\beta \stackrel{iid}{\sim}\text{Normal}(0,s)\) for some suitable standard deviation \(s\), depending on the scale of the linear predictor.

The vast majority of the distributions suggested by Latimer (2011) is also indexed by a number of ancillary parameters \(\boldsymbol\alpha\). The actual number of elements in \(\boldsymbol\alpha\) varies with the mathematical function. For instance, as is clear in Table 8.4, one extreme case is the Exponential distribution, which is only indexed by a rate parameter, modelled as in Equation 8.8 with \(g(\cdot) = \log(\cdot)\) and thus does not include any ancillary parameters. Using again Equation 8.3, we can see that the resulting hazard function for an Exponential distribution is \[ h(t\mid\mu_i) = \frac{\mu_i\exp(-\mu_i t_i)}{\exp(-\mu_i t_i)} = \mu_i, \] which means that, for each individual profile \(i\), the hazard is constant over time (and identical with the rate \(\mu_i\)) – cfr. the discussion in Section 2.2.3.

Similarly, when considering the Weibull, Gamma, Gompertz or log-logistic distributions, the linear predictor is still defined on the log scale, but there is also an additional shape parameter, whose presence makes these distributions much more flexible than the often too simplistic Exponential. In these cases, because the shape parameter is \(\alpha>0\), a suitable prior may be a relatively vague \(\text{Gamma}(\epsilon,\epsilon)\) for some small constant \(\epsilon\), say \(\epsilon=0.1\). The log-Normal distribution is also characterised by two parameters, but it is already defined on the log scale and thus the function \(g(\cdot)\) transforming the linear predictor is just the identity.

Note 8.4: The importance of being Bayesian (in survival modelling in HTA)

Latimer (2011) also mentions the Generalised Gamma and Generalised F as even more flexible options (the actual details of the mathematical definitions are not important, here – we also refer the reader to Jackson et al., 2010; and Jackson, 2016 and for more information).

These two distributions have, respectively, 2 and 3 ancillary parameters, which indeed contribute to making the shape of the resulting survival curve more “wiggly”. On the other hand, because of the larger number of free parameters, they tend to be “data-hungry” and it is generally harder to estimate all the parameters precisely.

In the case of the Generalised F, the ancillary parameters are \(\boldsymbol\alpha=(\sigma,p,q)\), representing a scale and two shape parameters, with \(\sigma,p>0\) and \(q\in \mathbb{R}\) – see Cox (2008) for more details.

Consider for instance the fictional data presented in Figure 8.2 (a). If we try to fit a Generalised F to the underlying data using MLE, we obtain the results presented in Table 8.5.

| Parameter | Mean | 2.5\% | 97.5\% |

|---|---|---|---|

| \(\mu\) | 2.291 | 2.135 | 2.448 |

| \(\sigma\) | 0.5873 | 0.4611 | 0.7481 |

| \(q\) | 0.8487 | 0.3575 | 1.34 |

| \(p\) | 0.002683 | 6.305505e-32 | 1.141320e+26 |

| Treatment | 0.3465 | 0.1744 | 0.5185 |

While running the model using MLE is very quick (the running time is only 0.107 seconds), there is an interesting finding in Table 8.5. The estimate for the parameter \(p\) has a 95% interval estimates that effectively spans over the entire \(\mathbb{R}^+\) range – the lower limit is effectively 0, while the upper limit is, for all intents and purposes, \(\infty\).

The reason for this quirky result is that there is not enough information in the data to be able to estimate properly all the model parameters – this is essentially a problem of “identifiability”.

Conversely, in the absence of substantial information coming from the data (which is often the case with censoring), we could use a Bayesian approach and set the priors to “nudge” the posterior in the right direction. For instance, we could set up the following relatively vague (and yet not totally clueless) priors: \(\sigma \sim \text{Gamma}(0.1,0.1)\), \(\log p\sim \text{Normal}(0,0.5)\) and \(q\sim\text{Normal}(0,2.5)\). Using this model structure, the results are pretty comparable with the MLE estimate for all the model parameters – except for \(p\), which this time has a rather different and most sensible estimate, both for the point and the interval values.

| Parameter | Mean | 2.5\% | 97.5\% |

|---|---|---|---|

| \(\mu\) | 2.2528 | 2.0758 | 2.4298 |

| \(\sigma\) | 0.5103 | 0.36953 | 0.6648 |

| \(q\) | 0.6859 | 0.02146 | 1.3037 |

| \(p\) | 1.1292 | 0.3758 | 2.5688 |

| Treatment | 0.3465 | 0.1798 | 0.519 |

The priors have the important effect of regularising the inference, by complementing the limited information contained in the data and placing suitably finite ranges for the parameters that are harder to identify, thus leading to a 95% estimate for \(p\) that is much more sensible. Notice, however, that similarly to our discussion in Example 6.3, none of these priors are extreme: using simple Normal theory or Monte Carlo simulations, we can see that the prior for \(\log p\) implies that \(\Pr(p<2.65)\approx 0.975\).

We may relax this assumption and increase the standard deviation for \(\log p\) and perhaps we should run a few versions of the model to assess the sensitivity of the results to changes in the priors; for instance, if we set \(\log p \sim \text{Normal}(0,1)\), then the posterior point estimate would change to 1.53 and the 95% posterior interval for \(p\) would expand up to 6.36. This does show some sensitivity to the prior, which is consistent with the failure of convergence in the MLE – but essentially, we need to do something, because pretending that the only information we have is sufficient, will simply return ridiculous (and potentially dangerous!) estimates, as in Table 8.5.

The advantages in the Bayesian approach come at a computational cost: the model now runs in 17.754 seconds – still not unbearable, but substantially higher than for the MLE equivalent. On this occasion2, clearly time well spent…

8.3.5 Bayesian computation for survival modelling in HTA

In theory, coding up a survival model in standard Bayesian software (e.g. BUGS or JAGS) is not that complicated, although this is one of the few places in which the syntax used by BUGS differ from that used by JAGS in dealing with censoring and thus care is needed when using either of these two pieces of software for survival modelling – see Lunn et al. (2013, sec. 12.6.2) for details in the syntax differences, as well as Alvares et al. (2021) for a detailed description of how JAGS can handle various types of survival models.

In addition, Gibbs sampling can struggle with survival models: compilation and running time can be rather long, mainly because the main outcome \(t\) has missing values in the data (the censored times). To combat this problem, it is generally useful to set initial values for \(t\) in a clever way to avoid problems in running the MCMC. In addition, convergence may be difficult to reach even with relatively simple models (e.g. Weibull Proportional Hazard).

For these reasons, survival modelling is one of the arguably limited number of applications in HTA in which the use alternative modes of Bayesian inference can be helpful to overcome or at least limit these issues. One option is to consider Integrated Nested Laplace Approximation (INLA – see Section 3.1.2). This is typically very fast and accurate, although, at present, it can only run a limited number of survival models (e.g. Weibull, Exponential, Gompertz, log-Normal and log-logistic).

Another important alternative is Hamiltonian Monte Carlo (HMC – see Section 3.1.2 and Section 2.3.3). HMC is typically very efficient and flexible for survival modelling and we can implement virtually any distributional assumption – the software Stan and the relevant R package rstan allow the user to build different blocks in which custom sampling distributions can be defined (which is helpful for instance to account for censoring – typically expressing the individual likelihood as in Equation 8.7). More details on Stan and rstan are given in Carpenter et al. (2017) and the comprehensive online user’s guide (Stan development team, 2024).

The code below shows an example, in which we construct a PH parameterisation for the Weibull distribution, starting from the AFT model described in Table 8.4, making use of Equation 8.9.

// Stan code for Weibull survival model (with PH parameterisation)

functions {

// Defines the log hazard (using the AFT parameterisation)

vector log_h (vector t, real shape, vector scale) {

vector[num_elements(t)] log_hvec;

// NB: The './' operator is the element-wise division

log_hvec = log(shape)+(shape-1)*log(t ./ scale)-log(scale);

return log_hvec;

}

// Defines the log survival (using the AFT parameterisation)

vector log_S (vector t, real shape, vector scale) {

vector[num_elements(t)] log_Svec;

for (i in 1:num_elements(t)) {

log_Svec[i] = -pow((t[i]/scale[i]),shape);

}

return log_Svec;

}

// Defines the sampling distribution (using the AFT parameterisation)

real surv_weibullPH_lpdf (vector t, vector d, real shape, vector scale) {

vector[num_elements(t)] log_lik;

real prob;

// NB: And the '.*' operator is the element-wise multiplication

log_lik = d .* log_h(t,shape,scale) + log_S(t,shape,scale);

prob = sum(log_lik);

return prob;

}

}

data {

int n; // number of observations

vector[n] t; // observed times

vector[n] d; // censoring (1=observed, 0=censored)

int K; // number of covariates

matrix[n,K] X; // matrix of covariates (n rows, K columns)

vector[K] mu_beta; // mean of the covariates coefficients

vector<lower=0> [K] sigma_beta; // sd of the covariates coefficients

real<lower=0> a_alpha; // parameters for the shape

real<lower=0> b_alpha;

}

parameters {

vector[K] beta; // Coefficients in linear predictor (with intercept)

real<lower=0> alpha; // shape parameter

}

transformed parameters {

vector[n] eta;

vector[n] mu;

eta = -(X*beta)/alpha; // rescales the linear predictor to get PH

for (i in 1:n) {

mu[i] = exp(eta[i]);

}

}

model {

alpha ~ gamma(a_alpha,b_alpha);

beta ~ normal(mu_beta,sigma_beta);

t ~ surv_weibullPH(d,alpha,mu);

}

generated quantities {

real scale; // scale parameter

scale = exp(beta[1]);

}A Stan programme is made by a number of “blocks”, each of which defines specific elements of the probabilistic model. Blocks are labelled by keywords (for instance functions, or data) and enclosed in curly brackets. Unlike in R, comments are indicated using the C++ syntax of double slash //.

In the example above, we start the code with a functions block, in which we define customised functions to be used in the sampling process. Here, we define the log hazard log_h() and the log survival log_S() functions. Unlike R, Stan requires the user to specify the type associated with each variable – for instance, the block

vector log_h (vector t, real shape, vector scale) {

...tells the compiler that inputs t, shape and scale are, respectively a vector, a real number and another vector; in addition we specify that the output value for the function log_h is also a vector.

In the functions block, we combine the log hazard and log survival functions to determine the individual likelihood contributions log_lik (again, in line with Equation 8.7). The function surv_weibullPH_lpdf() returns the sum of all the individual likelihood contributions into the real number prob, containing the overall log-likelihood – this effectively creates a new, custom-made distribution surv_weibullPH() that can be used to model sampling variability.

The next block defines the data. Here, we mostly need to explicitly specify the type (and length) of each data variable. The notation vector<lower=0> [K] sigma_beta instructs the compiler that the variable sigma_beta is a positive vector of length K.

Next, in the block parameters, we specify the type and dimension for all the core parameters, i.e. those that are directly modelled using a probability distributions. The parameters that are defined as deterministic functions of other (possibly random) quantities are all defined in the transformed parameters block. Here, for instance, we define the linear predictor (indicated as \(\eta_i\) in Equation 8.8 and as eta in the model code) using the relationship described in Equation 8.9.

The model block is where we specify the distributional assumptions: in this case, we set the prior distributions for the shape \(\alpha\sim\text{Gamma}(a_\alpha,b_\alpha)\) for set constants \(a_\alpha\) and \(b_\alpha\), as well as the coefficients for the linear predictor \(\beta_1,\ldots,\beta_K \stackrel{iid}{\sim} \text{Normal}(\mu_\beta,\sigma_\beta)\). Because the parameter beta is defined as a vector of size H in the model code, Stan understands the vectorised definition of the prior, which gives the same Normal with set mean \(\mu_\beta\) and standard deviation \(\sigma_\beta\) – notice that, unlike BUGS or JAGS, Stan indexes the Normal distribution more naturally in terms of mean and standard deviation. The variable t, representing the observed times is modelled using the custom-made surv_weibullPH distribution, which takes as inputs the vector of censoring indicators d, the shape alpha and the location parameter mu.

Finally, we can specify other generated quantities, which are typically functions of basic parameters, which are simply forward sampled – in this case we create a variable scale, which is the rescaled intercept in the linear predictor.

The code described above can be run from R using the package rstan. However, the vast majority of the relevant computational facilities for the specific objective of performing Bayesian modelling in HTA have been coded up into the package survHE, which we use in the rest of the chapter and introduce in Section 8.4.

8.4 Using the R package survHE

survHE (Baio, 2020) is an R package designed with the specific objective to perform survival analysis for HTA. In a nutshell, survHE is designed as a modular package, with a basic component (the actual survHE package), which is essentially a “wrapper” to one of the most popular survival packages, flexsurv (Jackson, 2016), which is a general-purpose tool for performing several types of survival analysis using maximum likelihood estimates. The core survHE package also defines several facilities that are helpful when performing the analysis in an HTA context, including standardised post-processing of the estimates, both in tabular and graphical format, as well as for the purposes of PSA (Section 4.3).

There are also two “add-on” packages, called survHEinla and survHEhmc, which code specific functions to run Bayesian survival modelling, using either INLA or HMC through Stan and rstan.

Depending on the user’s specification, survHE maps internally to different code, which calls either flexsurv, rstan or INLA in the background to produce the relevant estimates. The resulting output is also standardised and presented in a form that is common, irrespective on the underlying inferential engine. Further post-processing can happen directly in R.

We use NICE TA174 as a running example to demonstrate the use of survHE to perform Bayesian modelling in the context of survival analysis in HTA. Of course, the use of survHE is absolutely not a necessity and the user could write bespoke code to run the MCMC analysis (either in BUGS/JAGS or in Stan).

Nonetheless, we do take advantage of the fact that survHE is somehow tailor-made for this specific context and thus use it throughout. We also refer the user to Baio (2020), as well as the package website (https://gianluca.statistica.it/software/survhe/) and GitHub repository (https://github.com/giabaio/survHEhmc) for further information.

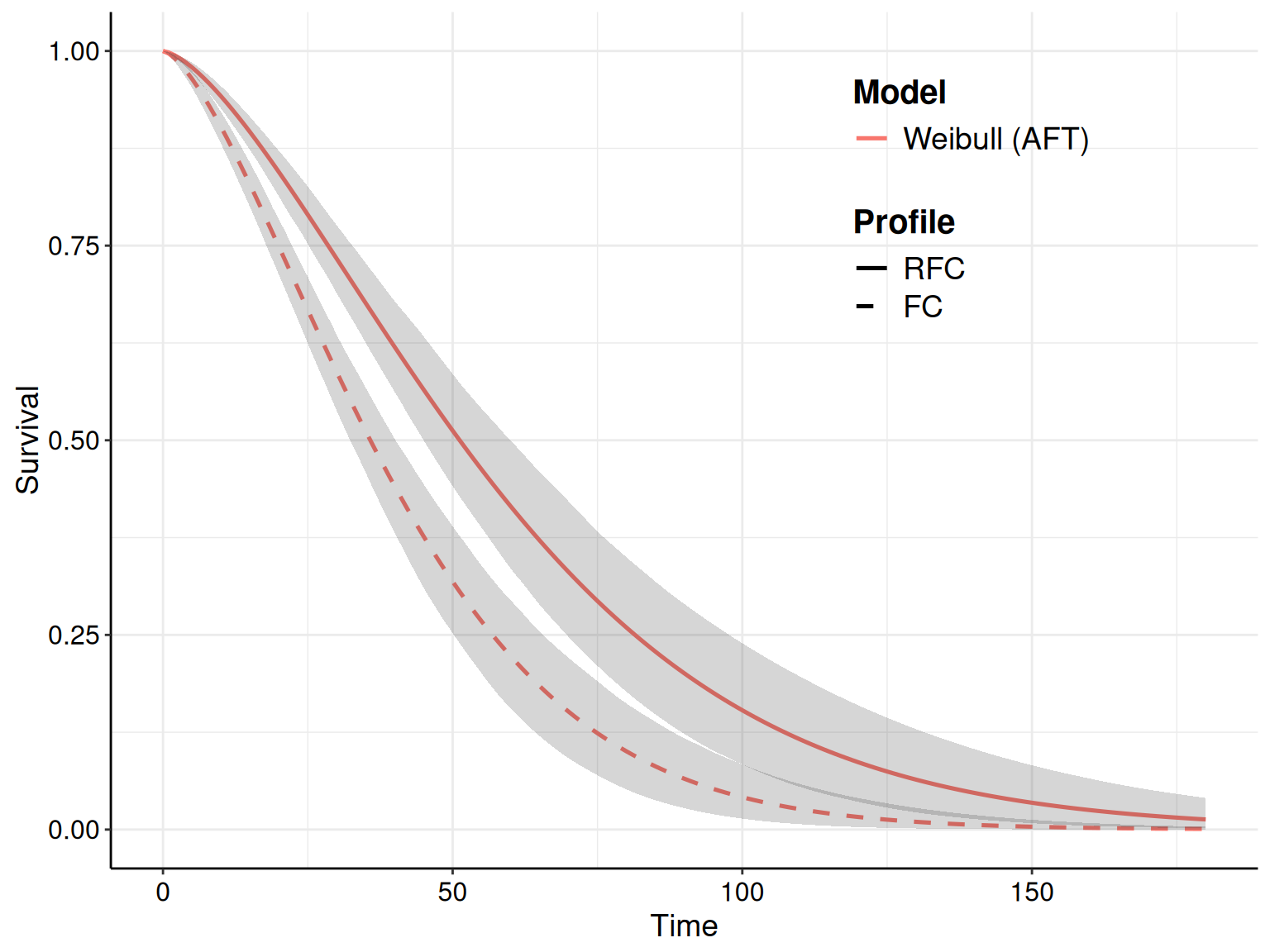

Example 8.2. NICE TA174 (continued): running the models using survHE. We use survHE to fit a Bayesian model using different distributional assumptions to the NICE TA174 data described in Example 8.1. To fix ideas, we consider three options. The first one is a Weibull (AFT) model, specified as in Equation 8.10.

\[ \begin{aligned} t_i &\sim\text{Weibull}(\mu_i,\alpha) \\ \log(\mu_i) & = \beta_0 + \beta_1 \text{Treatment}_i \\ \beta_0,\beta_1 & \stackrel{iid}{\sim}\text{Normal}(0,5) \\ \alpha & \sim \text{Gamma}(0.1,0.1). \end{aligned} \tag{8.10}\]

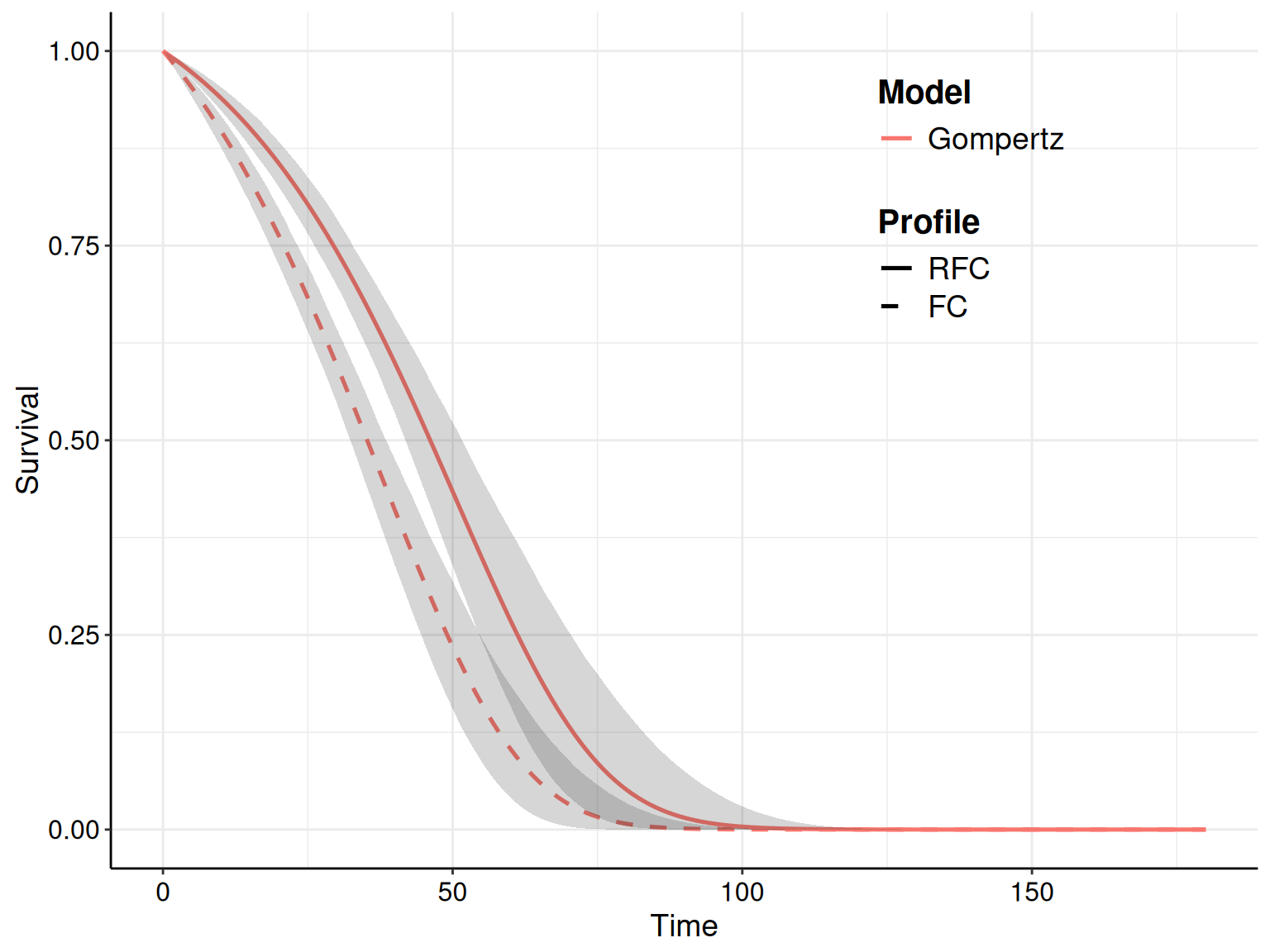

For the second model, we use a similar specification, but choose a Gompertz sampling distribution, as in Equation 8.11.

\[ \begin{aligned} t_i &\sim\text{Gompertz}(\mu_i,\alpha) \\ \log(\mu_i) & = \beta_0 + \beta_1 \text{Treatment}_i \\ \beta_0,\beta_1 & \stackrel{iid}{\sim}\text{Normal}(0,5) \\ \alpha & \sim \text{Gamma}(0.1,0.1). \end{aligned} \tag{8.11}\]

Finally, we specify a log-Normal model, as in Equation 8.12.

\[ \begin{aligned} t_i &\sim\text{log-Normal}(\mu_i,\alpha) \\ \mu_i & = \beta_0 + \beta_1 \text{Treatment}_i \\ \beta_0,\beta_1 & \stackrel{iid}{\sim}\text{Normal}(0,100) \\ \log(\alpha) & \sim \text{Uniform}(0,5). \end{aligned} \tag{8.12}\]

Notice that the prior distributions set out for the model parameters in the three specifications are the ones used by default by survHE – see Baio (2020) and Section 8.4.1 for more details.

We can use the function fit.models() in the package survHE to run the three models using Stan and rstan in the background, for instance using code such as the following.

# Runs the Bayesian analysis using 'survHE'

m=fit.models(

Surv(time,status)~treatment,

data=data,

distr=c("wei","gom","lno"),

method="hmc"

) fit.models() takes as input:

- a model “formula”, in which we specify the outcome

Surv(time,status), indicating the observed times and the censoring indicator, as a function of the linear predictor. In this case, we only include the treatment arm as a covariate (technically, this is a “factor”, i.e. a categorical variable, taking valuesRFCandFC) and, in line with standardRnotation, we can omit the intercept, which we could explicitly add or remove by writingSurv(time,status)~1+treatmentorSurv(time,status)~treatment-1, respectively, as it is included by default. - A named dataset (in this case, we assume that the subset for the TA174 data shown in Figure 8.3 is stored in an object named

data). - A vector of named distributions.

survHEhas a set of built-in abbreviations3 – the string vectorc("wei","gom","lno")instructsRto run the models for the three sampling distributions specified in Equations 8.10–8.12. It is not essential to store multiple models in the same object (m, in this case). We could have run three separate instances offit.models()giving as input a different distribution, in each. - The inferential method, in this case

hmc. The default considers the MLE.

A potentially helpful optional argument is save.stan; if set to TRUE, when method="hmc", then survHE will save the pre-compiled Stan model code on the user’s working directory. This can then be used to customise the model further, starting from the working template that is built-in the survHE package.

The object m contains the output generated for the three models considered; in particular, it contains four components, as can be seen by typing the R command names(m). The first one (models) is the object in which survHE stores the output produced by the underlying inferential engine (in this case, rstan). survHE has a number of methods that can be applied to this object, in order to print and plot the outcome in suitable formats.

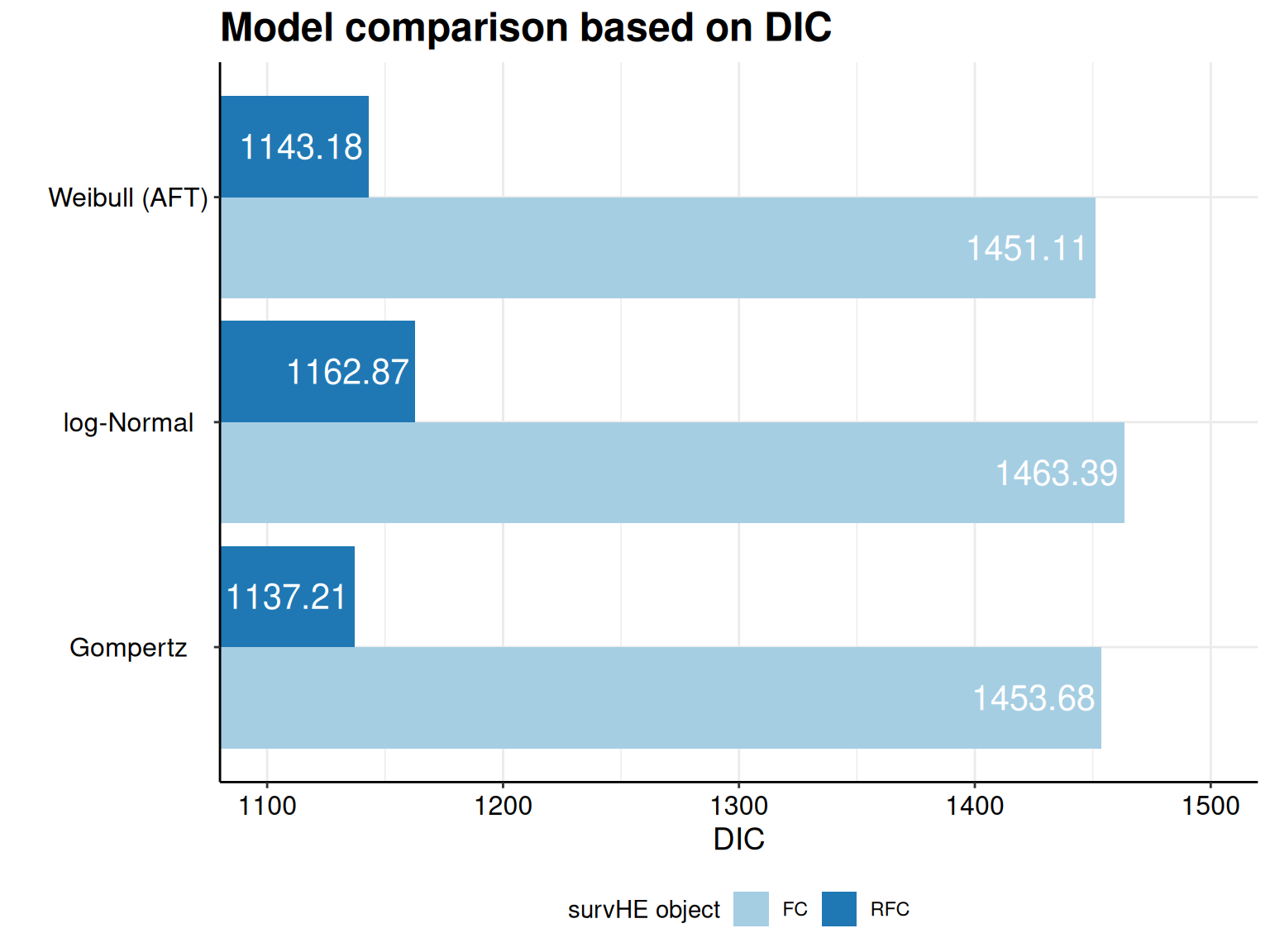

The second element of m is the object model.fitting, which contains a set of model fitting statistics, i.e. the AIC and BIC, as well as the DIC, if the model has been fitted using a Bayesian method – see Section 5.3.1 for more details on information criteria.

The other two objects, which can be accessed using the notation m$method and m$misc are really just for survHE internal consumption and contain a string with the inferential method used (hmc, in this case) and a set of “miscellanea”, including the actual data object, the running time (in seconds) and the formula specified to fit the model. As mentioned above, the user does not really need to use this information, but other functions in survHE do, in order to create plots and relevant summaries.

We can summarise the models using the print() method, for instance using the following code.

# Prints the summary stats for the first model (Weibul AFT)

print(m,mod=1)

Model fit for the Weibull AF model, obtained using Stan (Bayesian inference via

Hamiltonian Monte Carlo). Running time: 2.812 seconds

mean se L95% U95%

shape 1.503300 0.0831493 1.347573 1.677060

scale 45.818701 2.9156988 40.743698 52.171665

treatmentRFC 0.359966 0.0844154 0.197548 0.527928

Model fitting summaries

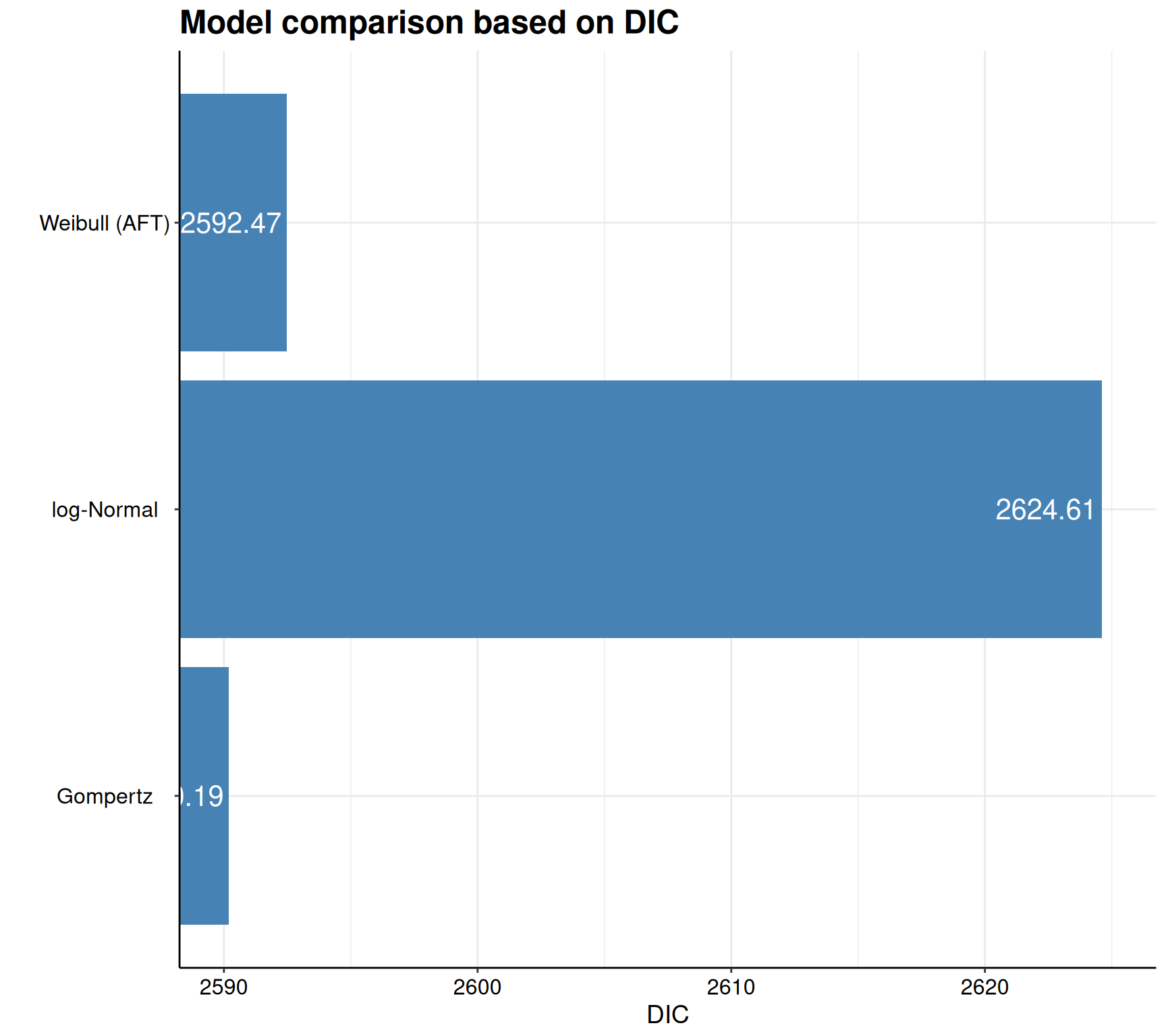

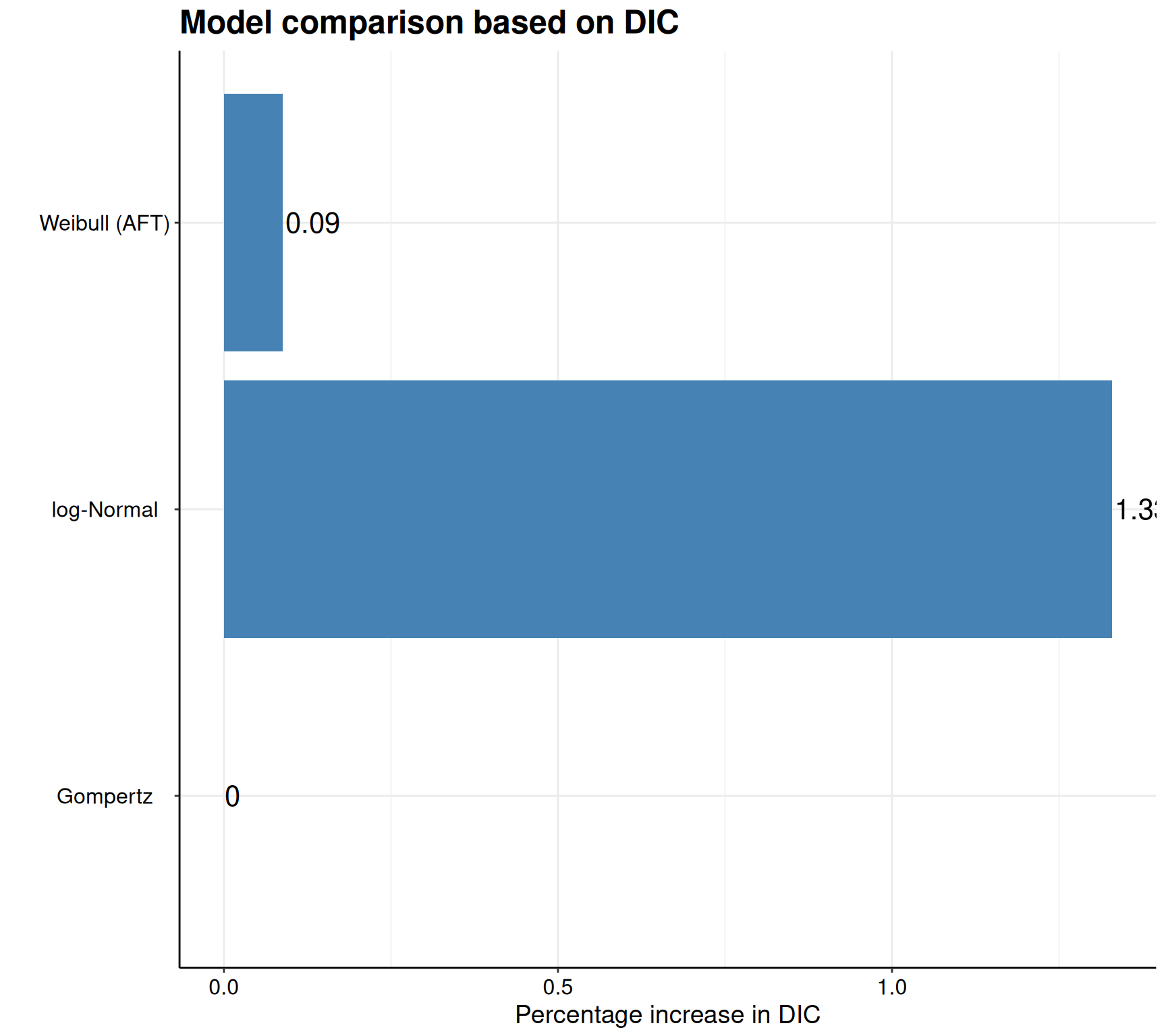

Akaike Information Criterion (AIC)....: 2594.706

Bayesian Information Criterion (BIC)..: 2613.494

Deviance Information Criterion (DIC)..: 2592.466# Prints the summary stats for the second model (Gompertz)

print(m,mod=2)

Model fit for the Gompertz model, obtained using Stan (Bayesian inference via

Hamiltonian Monte Carlo). Running time: 3.388 seconds

mean se L95% U95%

shape 0.04151213 0.00618017 0.02866643 0.0533706

rate 0.00876049 0.00119050 0.00666817 0.0113323

treatmentRFC -0.55877128 0.12869304 -0.81108868 -0.3021874

Model fitting summaries

Akaike Information Criterion (AIC)....: 2591.919

Bayesian Information Criterion (BIC)..: 2610.707

Deviance Information Criterion (DIC)..: 2590.191# Prints the summary stats for the third model (log-Normal)

print(m,mod=3)

Model fit for the log-Normal model, obtained using Stan (Bayesian inference via

Hamiltonian Monte Carlo). Running time: 4.378 seconds

mean se L95% U95%

meanlog 3.731241 0.0856571 3.575029 3.913652

sdlog 1.216616 0.0597203 1.108305 1.342406

treatmentRFC 0.430394 0.1074018 0.215014 0.632575

Model fitting summaries

Akaike Information Criterion (AIC)....: 2626.812

Bayesian Information Criterion (BIC)..: 2645.600

Deviance Information Criterion (DIC)..: 2624.612As is possible to see, the print() method in survHE returns a standardised table (this is independent on the inferential method chosen) and reports some key information. First, it specifies what model has been fitted and with which inferential method, as well as the running time (extracted from the object m$misc$time2run). Then, the table shows the point estimate for the model parameters, as well as a measure of standard error and a 95% interval. As we are using a Bayesian model, here, these are obtained by summarising the HMC simulations from the posterior distributions. Finally, the print() method provides some model fitting statistics – as this is a Bayesian model, AIC, BIC and DIC are all computed and reported.

One interesting aspect from the summary tables above is that the coefficients of the models are estimated to substantially different values. This is not surprising for the core parameters: for instance, the parameter scale in the Weibull AFT model is the intercept \(\beta_0\) of the linear predictor \(\eta_i=\beta_0+ \beta_1 \text{Treatment}_i\). In the Gompertz model, \(\beta_0\) is still the intercept of \(\eta_i\), but in this model it represents a rate, instead of a scale – effectively, it is defined on an inverse scale as \(\text{rate}=1/\text{scale}\). In the log-Normal model, \(\beta_0\) is simply the mean survival time, on the log scale, for individuals over which there is no treatment effect (i.e. the controls) and thus the interpretation is also different, which explains the difference in the estimated value.

Similarly, the nuisance parameters \(\alpha\) represents a shape for the Weibull and Gompertz (albeit in regard to a scale and a rate, respectively), while it is a log standard deviation for the log-Normal model, which again justifies the different values shown in the summary tables above.

As for the treatment effect, the Weibull and the log-Normal models described above are both characterised by an AFT interpretation. This explains why the resulting coefficient for the treatment effect (indicated as treatmentRFC in the summary tables and equivalent to \(\beta_1\) in the models of Equations 8.10 – 8.12) are reasonably similar, at least in the point estimate. The Gompertz model, conversely, has a PH interpretation, whereby \(\exp(\beta_1)\) is the hazard ratio, i.e. a measure of how much more likely a random individual from the target population is to experience the event under study if they are in the treatment arm, as opposed to the control. In this case, we can see that \(\exp(\beta_1) = \exp(-0.5587713) = 0.572\) indicates that the intervention arm (RFC) is beneficial as it decreases the hazard of experiencing the event (progression) – this is because the hazard ratio is less than 1.

Consistently with this finding and the discussion in Note 8.3 in Section 8.3.3, the acceleration factor for both the Weibull and the log-Normal models is positive, to indicate a beneficial treatment effect.

8.4.1 Setting prior distributions

One of the main advantages of survHE is that, similarly to other packages that use rstan in the background (e.g. the very popular brms – see Bürkner, 2017), the user does not have to code up a full Bayesian model using Stan code. Rather, for a set of defined models, the package “pre-compiles” the code (which makes the running time shorter, overall) and the user needs to specify commands similar to the R built-in function lm() to define the distributional assumptions and data, in order to run the analysis.

On the one hand, this is a very attractive feature, because it removes a potential barrier for the user, thus possibly improving uptake of the Bayesian machinery in complex cases. On the other hand, however, this somehow constrains the modelling to a more or less pre-defined setup, which may limit the generalisability and use of the tool.

Fortunately, neither these potential issues are insurmountable: for survHE, the average user can probably use the default setup (with the usual caveat that extensive post-processing and sensitivity analysis are essential to any statistical modelling, perhaps even more so in a Bayesian context). In addition, the package has some built-in facilities that allow to modify the default code as well as the default prior distributions.

Example 8.3. NICE TA174 (continued): setting non-default priors. If we are happy with the distributional assumptions specified in the default models encoded in survHE (e.g. considering a Normal distribution for the linear predictor coefficients \(\boldsymbol\beta\), or a Gamma prior for the shape \(\alpha\) of the Weibull distribution), we can use the optional argument priors to instruct fit.models() to use customised values for the parameters of these distributions (see Baio, 2020 for more details on how to define this argument).

For instance, suppose we want to model the shape parameter for the Weibull model using an Exponential(3) distribution. By the properties of the Gamma distribution, this is equivalent to modelling \(\alpha \sim \text{Gamma}(1,3)\). In addition, we want to change the prior for the regression coefficients to \(\beta_0,\beta_1\stackrel{iid}{\sim}\text{Normal}(0,10)\), to double the standard deviation from the default choice. We can specify this version of the model using the following command – see again Baio (2020, sect. 5.2) specifically on how to structure the list priors in the presence of multiple distributions specified in the input distr, in the call to fit.models().

m1=fit.models(

Surv(time,status)~treatment, data=data, distr="wei", method="hmc",

priors=list(

wei=list(

a_alpha=1,b_alpha=3,

sigma_beta=rep(10,2)

)

)

)Here, we need to specify sigma_beta=rep(10,2) because the vector of regression coefficients \(\boldsymbol\beta\) has two values (\(\beta_0,\beta_1\)). We do not have to assume the same standard deviation for all the elements of \(\boldsymbol\beta\) and we could have set a vector of different values, e.g. sigma_beta=c(1,4).

In this particular instance, the output of the model does not vary dramatically, as we can check by comparing the summary tables (cfr. the results in Example 8.2).

# Prints the results with the revised priors

print(m1)

Model fit for the Weibull AF model, obtained using Stan (Bayesian inference via

Hamiltonian Monte Carlo). Running time: 2.813 seconds

mean se L95% U95%

shape 1.482768 0.0842161 1.325749 1.653637

scale 46.331412 3.1413481 40.868067 53.206608

treatmentRFC 0.360265 0.0862086 0.191665 0.537569

Model fitting summaries

Akaike Information Criterion (AIC)....: 2594.828

Bayesian Information Criterion (BIC)..: 2613.616

Deviance Information Criterion (DIC)..: 2592.902If we wanted to completely change the distributional assumptions for the priors, then we would need to set the save.stan option to TRUE in a dummy call to the fit.models() function and save the model template to a .stan file. The resulting object, say x, would also include an element x$misc$data.stan, which is a list with the relevant data formatted in a way that rstan would accept. At that point, we can modify the Stan code directly – for instance we could replace the code

model {

alpha ~ gamma(a_alpha,b_alpha);

...

}with the code

model {

alpha ~ normal(0,3);

...

}to encode the assumption that the shape parameter for the Weibull AFT model has a Half-Normal distribution, i.e. a Normal truncated to be positive – because we have specified in the parameters block

real<lower=0> alpha;then Stan knows that alpha must be positive and thus can automatically rescale the set distribution to fit the range for the parameter. Notice however that, in this case, we cannot run the model using survHE, but we would need to use pure rstan to specify data and model code see the rstan manual (Stan development team, 2024), for details on how to do so.

8.4.2 Assessing model convergence

Much as for any Bayesian model, before we can use the output of a call to fit.models() that specifies method="hmc", we need to perform extensive model diagnostics to check convergence and autocorrelation, as discussed in Section 2.3.2. This is fundamental, because of course we need to make sure that the estimates are representative of the target posterior distribution, before we can use them to derive the important quantities for the HTA analysis, e.g. the survival curves.

We can use a combination of survHE and rstan (and, possibly, bmhe) facilities to streamline this process, as demonstrated in the next example.

Example 8.4. NICE TA174 (continued): assessing model convergence. Outputs obtained running survHE are saved onto the R workspace as objects in the survHE class. As mentioned above, these are effectively lists with several elements, one of which, model, in fact contains all the output generated by the underlying inferential engine. Because in the object m described in Example 8.2 is created running rstan in the background, we can use all the rstan features to assess convergence, much as we have discussed in Section 2.3.2.

Firstly, the print() method in survHE has an option that allows to show the original, “unstandardised” results obtained by the package that has been called in the background to perform the analyses (this would be flexsurv for MLE, or Stan/INLA for a Bayesian model). We can do this by using the option original=TRUE, as in the following code.

print(m,mod=2,original=TRUE,digits=2,print_priors=TRUE)Inference for Stan model: Gompertz.

2 chains, each with iter=2000; warmup=1000; thin=1;

post-warmup draws per chain=1000, total post-warmup draws=2000.

mean se_mean sd 2.5% 25% 50% 75% 97.5% n_eff Rhat

beta[1] -4.75 0.00 0.13 -5.01 -4.84 -4.75 -4.66 -4.48 803 1.00

beta[2] -0.56 0.00 0.13 -0.81 -0.65 -0.56 -0.47 -0.30 1005 1.00

alpha 0.04 0.00 0.01 0.03 0.04 0.04 0.05 0.05 838 1.00

rate 0.01 0.00 0.00 0.01 0.01 0.01 0.01 0.01 809 1.00

lp__ -1294.31 0.05 1.26 -1297.51 -1294.89 -1294.00 -1293.37 -1292.85 629 1.01

Samples were drawn using NUTS(diag_e) at Tue May 26 17:05:59 2026.

For each parameter, n_eff is a crude measure of effective sample size,

and Rhat is the potential scale reduction factor on split chains (at

convergence, Rhat=1).

Prior modelling assumptions

alpha ~ gamma(0.1, 0.1)

(Intercept): beta[1] ~ normal(0, 5)

treatmentRFC: beta[2] ~ normal(0, 5)

t ~ surv_gompertz(d,alpha,mu)The output is a summary table where the parameters are named using the convention defined in the Stan code that is automatically used by survHE when calling rstan in the background. In this case, the coefficients are presented on the log scale, which is how the linear predictor is defined in the Stan code. The parameter beta[1] maps onto the log of the parameter rate, while beta[2] maps onto the parameter treatmentRFC presented in the summary table shown in Example 8.2. The parameter alpha is the shape in Example 8.2. In the Stan code, the rate is also directly computed (in fact, in the generated quantities block – cfr. the code discussed in Section 8.3.5).

The original table also shows familiar quantities such as n_eff and Rhat that can be used to check convergence and autocorrelation (see Section 2.3.2). In this case, we have also used the option print_priors=TRUE, which, in combination with original=TRUE, instructs survHE to append a summary of the distributional assumptions used in the prior distributions to the table. This option can be omitted and obviously has no effect when the model is run using flexsurv.

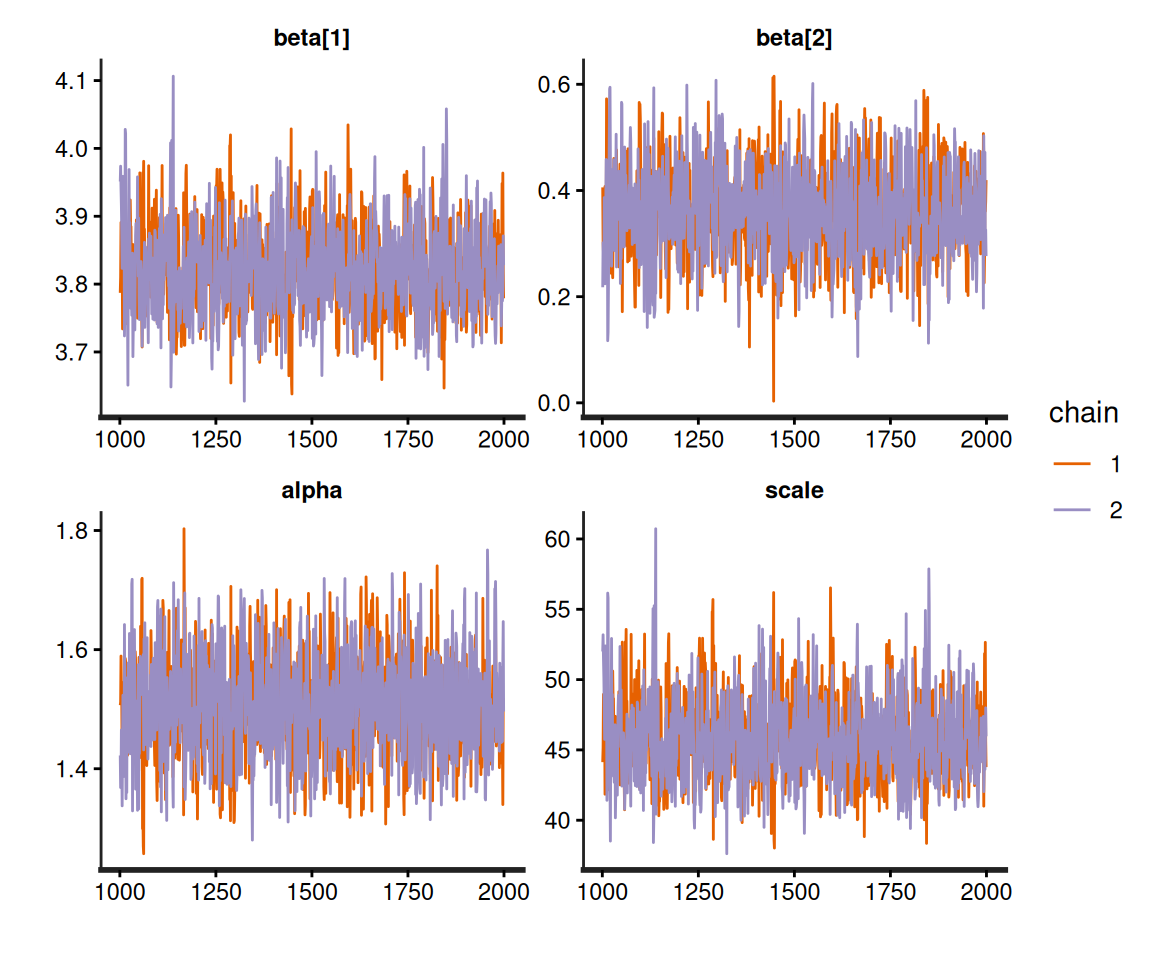

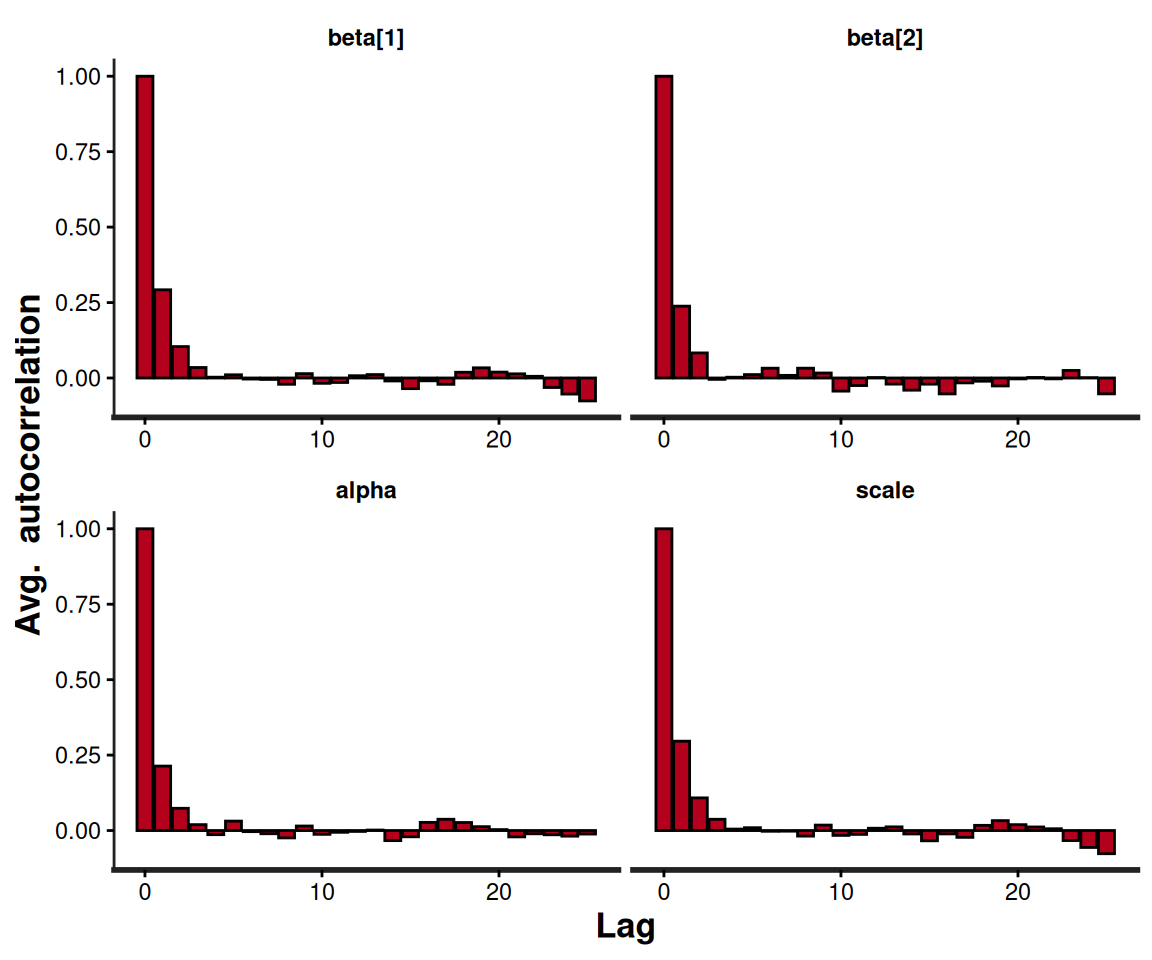

In addition, as mentioned above, we can use rstan built-in functions to visualise and assess convergence, for example as in the following code and the resulting output in Figure 8.4.

# Generates traceplots for the Weibull model's parameters

rstan::traceplot(m$models[[1]])

# Generates autocorrelation plots for the Weibull model's parameters

rstan::stan_ac(m$models[[1]])

Stan object.

Stan object.

This sort of diagnostic checks should always be performed when running Bayesian modelling, but, again, there is no overheads in carrying them out following a survHE run, because the resulting object is, fundamentally, a rstan output and thus all “standard” Bayesian procedures for post-processing directly apply.

8.4.3 Visualisation and assessment of the survival curves

Once a model has been fitted to observed data and the estimates for the model parameters obtained (e.g. in terms of simulations from the joint posterior distribution, in a Bayesian context), we need to move our analysis to a slightly different level, in which we try and get a sense of the treatment effect, in terms of improvement in survival.

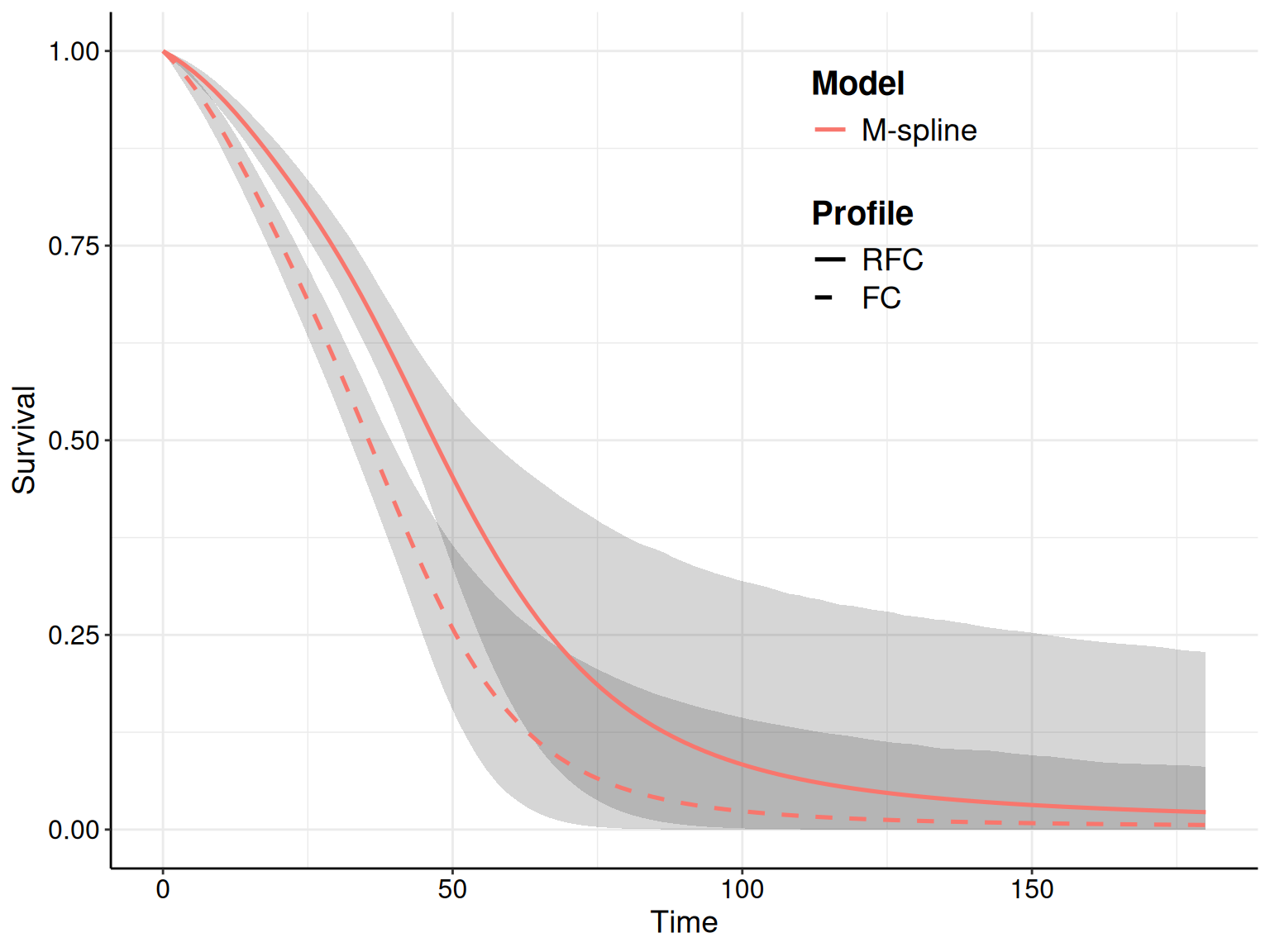

As mentioned in Section 8.3, the main reason why we focus on parametric modelling is because we can use the posterior for the model parameters \(\boldsymbol\theta\) to induce a posterior on the survival curve \(S(t\mid\boldsymbol\theta)=g(\boldsymbol\theta)\), where the function \(g(\cdot)\) depends on the specific model chosen, as shown in Table 8.4.

Especially as the general guideline is to try a number of parametric models to then produce the “base-case” evaluation using the one that “fits the data best” (we clarify the actual meaning of this phrase in the next few sections), it is vital to visualise the results and be able to argue for a specific choice of model, on a combination of numerical and clinical evidence.

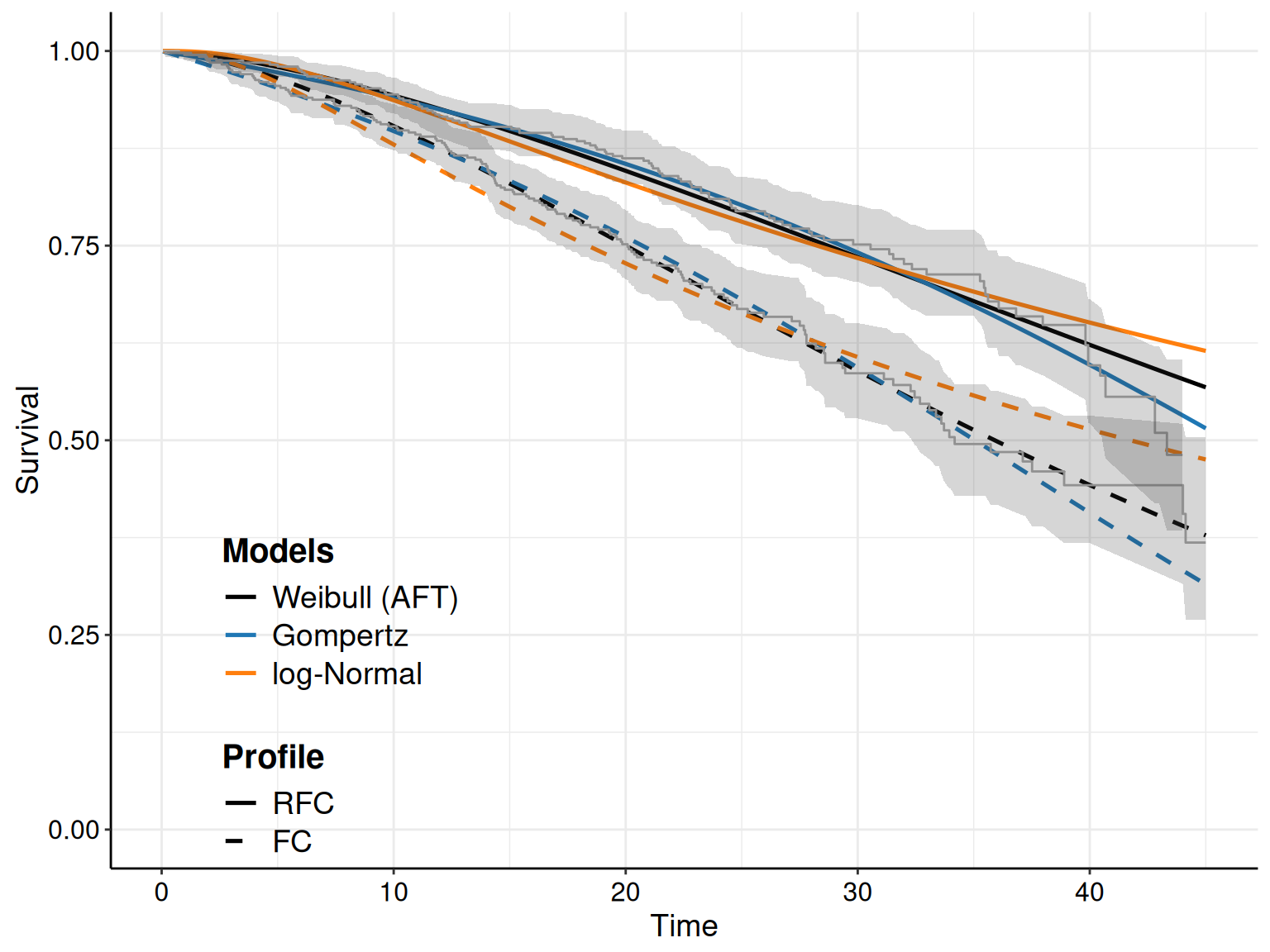

Example 8.5. NICE TA174 (continued): estimating the survival curves. survHE has a built-in plot() method, which is based on ggplot2 and can be used to visualise the resulting survival curve for the models fitted using the function fit.models(). For instance, in the NICE TA174 example, we can simply use the following code – notice that we take advantage of the ggplot2 processing facilities and overwrite survHE colouring scheme to ensure that the three models are most distinguishable both when visualised in colour and in grey-scale. We do this by adding the ggplot2 function scale_color_manual() and specifying colours with significant differences in luminance, which are then markedly separated in grey-scale.

# Plots the survival curves for all models and adds some customisation

plot(

m,

# Adds the KM estimates (optional)

add.km=TRUE,

# Customises the treatment labels (optional)

lab.profile=c("RFC","FC")

) +

# Customises the position of the legend (optional)

theme(

legend.position.inside=c(.2,.2)

) + scale_color_manual(values=c("#000000","#1F77B4","#FF7F0E"))

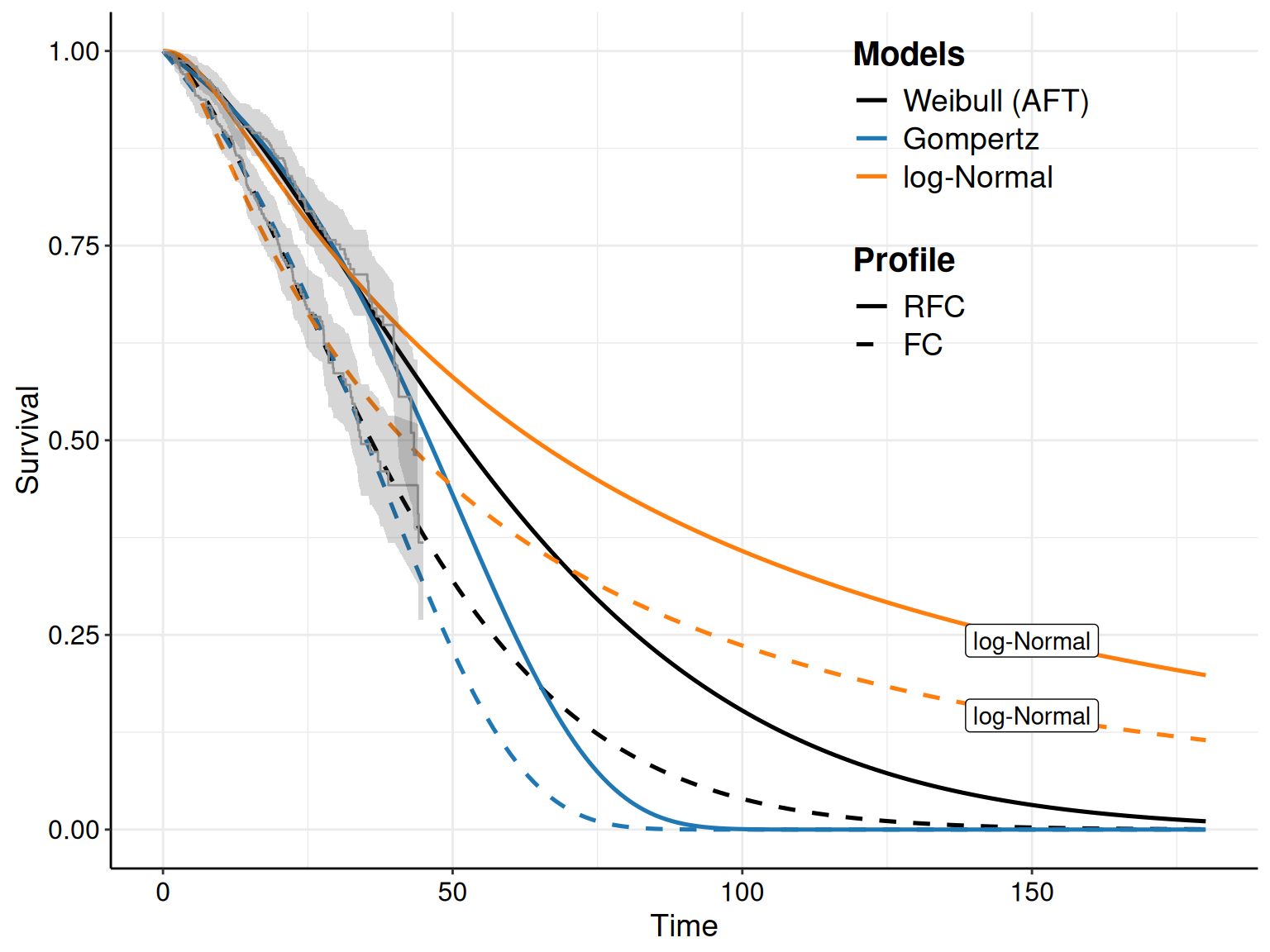

Figure 8.5 shows the KM curves for the two treatment arms with the survival curves estimated from the models in Equations 8.10 – 8.12. Typically, we seek the model that tends to approximate the trajectory in the KM best: for instance, in Figure 8.5 the log-Normal model seems relatively badly calibrated, particularly in the FC arm, where it under-estimates the survival pattern, especially at the beginning of the observation (when the curve is outside the interval around the KM estimates). It also seem to slightly over-estimate survival towards the end of the trial, although in this case the curve is within the KM interval.

As for the other models, the Gompertz does reasonably well for the RFC arm, seemingly capturing the dip in survival at the end of the follow-up. In the FC arm, it perhaps tends to under-estimate survival at the end of the follow-up, perhaps due to some sort of “plateau”, probably due to censoring.

The Weibull model seems perhaps to adapt best to the FC arm, especially at the end of the follow-up, but it is maybe a bit over-optimistic in the last part of the observed data, for the RFC arm.

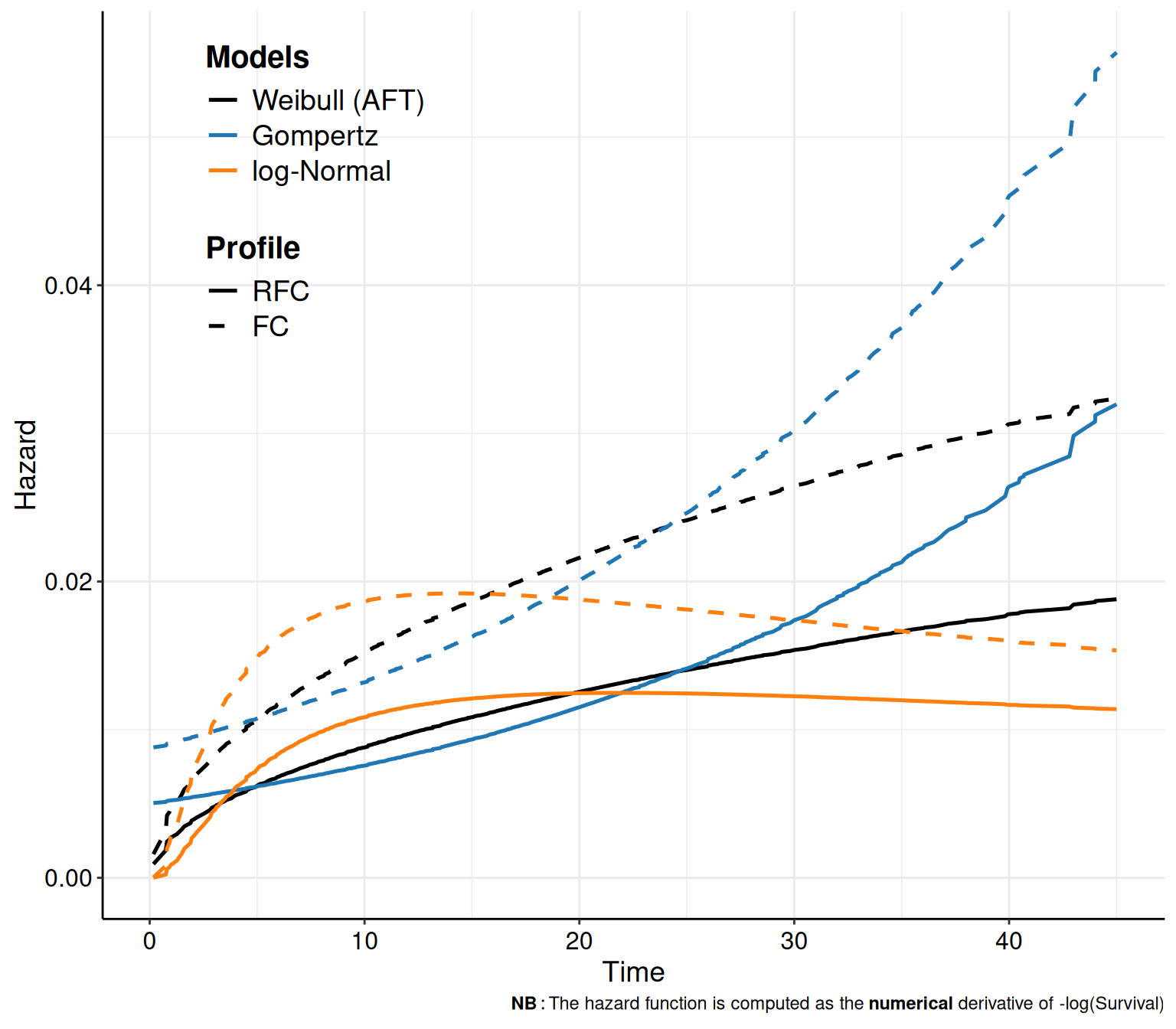

While perhaps the main objective of the survival analysis in HTA is to produce an estimate of the survival curves, it is generally very helpful to also look at the resulting hazards, to get a sense of the clinical plausibility of the results.

The hazard functions tell us about the instantaneous (and cumulative) risk of experience the event – for instance, it is possible that the risk of dying is very high immediately after a given surgery, but then stabilises or even decreases, over time. Or: it may be completely unrealistic that, with time passing, the risk of a given clinical event becomes lower. These considerations should be used to assess the meaningfulness of alternative model specifications.

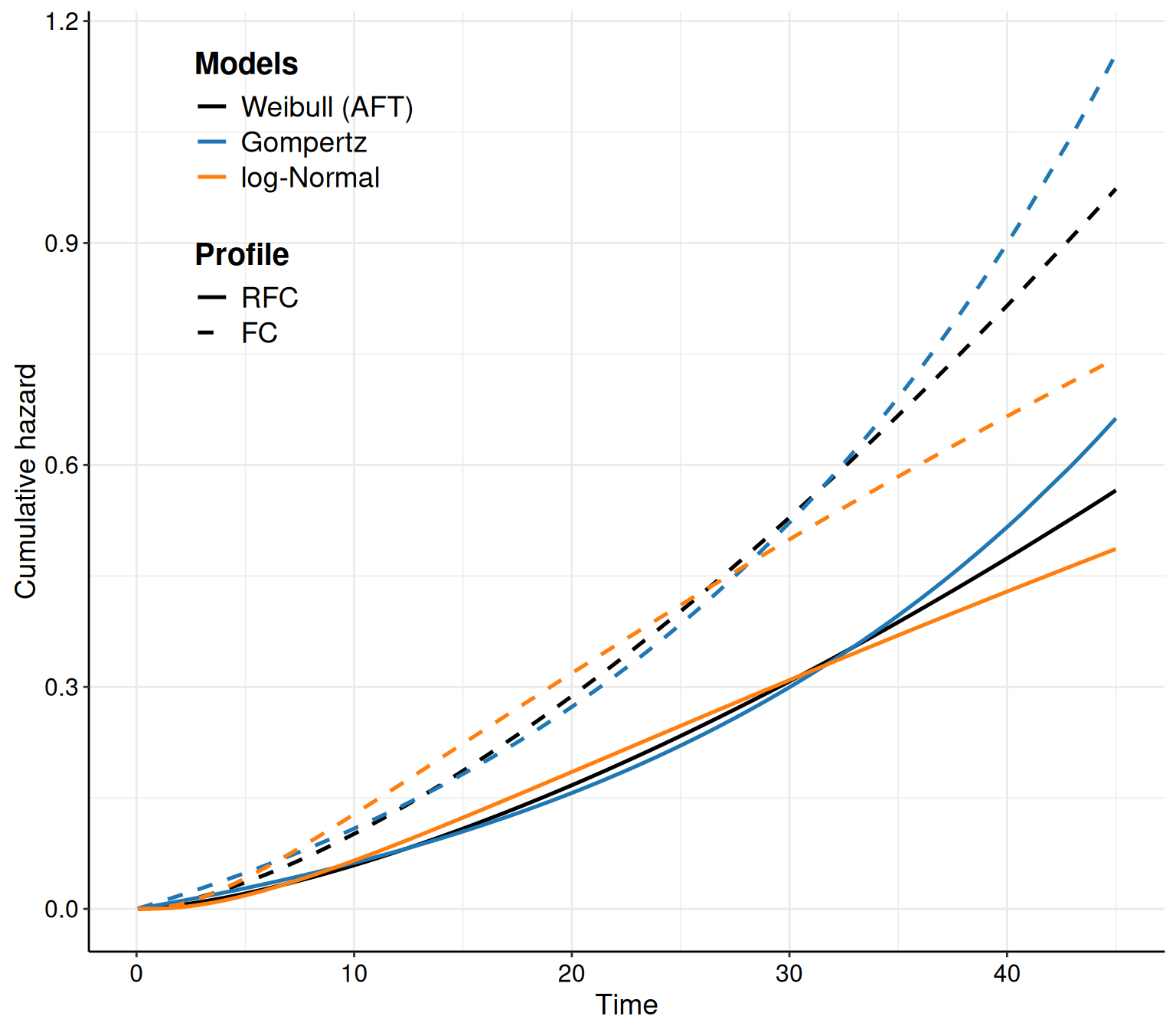

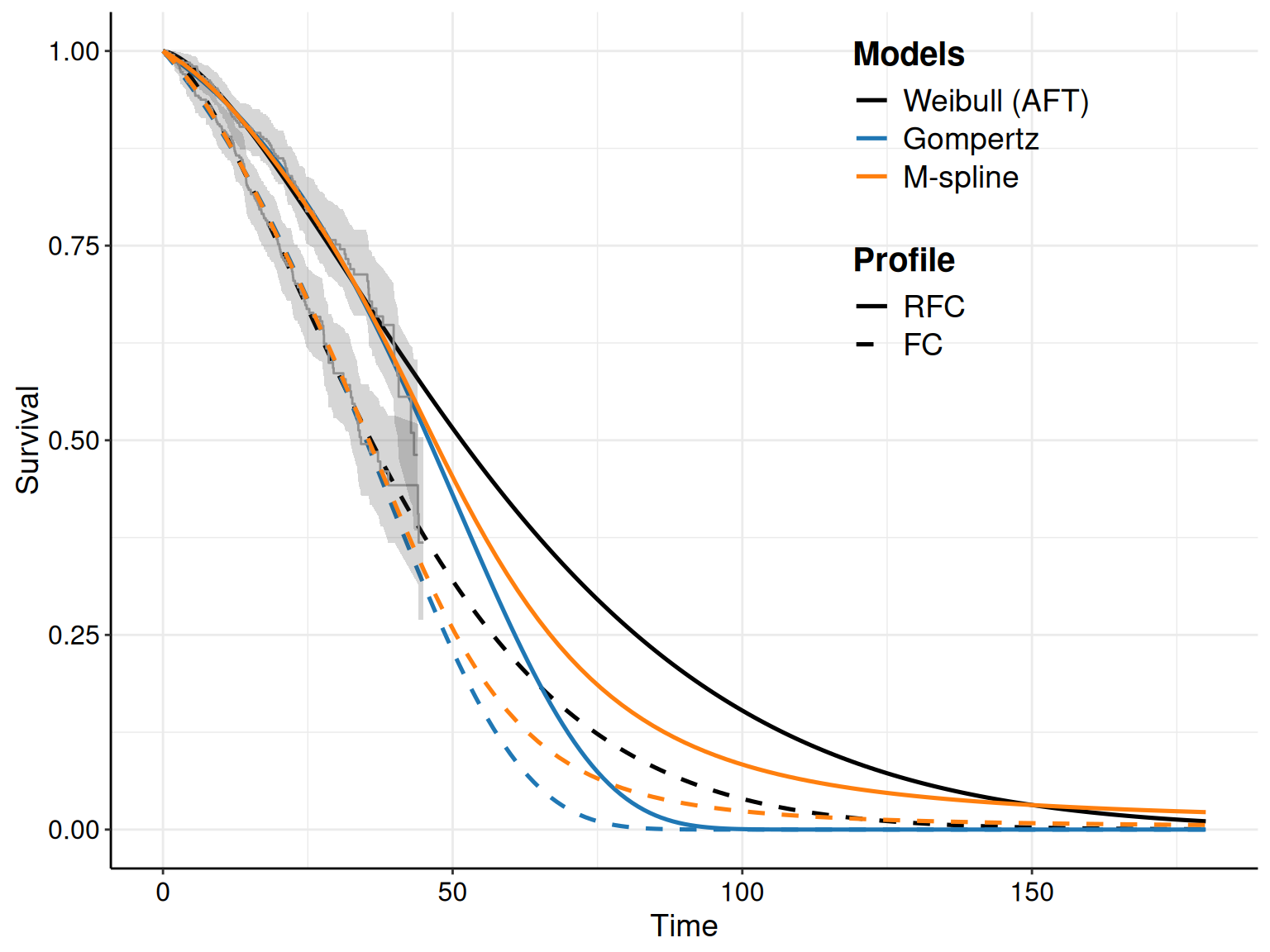

In survHE, we can also plot the hazard and cumulative hazard functions adding the option what="hazard" or what="cumhazard" to the call to the plot() method. The latter (Figure 8.6 (b)) is simply computed using Equation 8.6. The former (Figure 8.6 (a)) is computed as the numerical derivative of \(-\log S(t\mid\boldsymbol\theta)\).

Example 8.6. NICE TA174 (continued): estimating the hazard curves. Figure 8.6 shows the hazard functions derived from the models in Equations 8.10 – 8.12. In Figure 8.6 (a) it is possible to see how the hazard function has a big increase towards the end of the observation period, while it actually decreases for the log-Normal model. While these are related to the mathematical functions describing these two distributions, it is also helpful to compare the trajectories with clinical knowledge about the underlying disease.

Very often, studies based on survival analysis in HTA tend to report graphs such as that in Figure 8.5; these are arguably very important and useful and should be used as the basis for comparison and assessment of model fit and plausibility. However, as they are the output of a statistical modelling, we know that they are subject to inherent uncertainty, because the underlying model parameters are. Thus, it is also important to report a measure of implied uncertainty on the average survival curves.

This is naturally embedded in survHE, which simply needs to add the option nsim to the call for the plot() method. This instructs R to not just take into account the point estimates and plug the relevant values to compute the survival curves; rather, in a full Bayesian approach (particularly when using HMC), we can use the simulations from the joint posterior distribution of all the model parameters \(\boldsymbol\theta\) and propagate the uncertainty to the implied distribution of the survival curve \(S(t\mid\boldsymbol\theta)\).

If the input nsim is set to a value greater than 1, then survHE will automatically construct simulations for the entire distribution of the underlying survival curves. Technically, this automatically calls in the background another survHE function, make.surv(), which produces the required number of simulations.

NoteThe importance of being Bayesian (in survival modelling in HTA) – again

While, strictly speaking, assessing fully the uncertainty in model outputs is not a Bayesian feature only, arguably, the Bayesian philosophy and machinery make this perhaps their key aspect – as discussed in Chapters 1, 2 and 4, the main object of the inference, within a Bayesian approach, is directly the joint posterior distribution, which we can summarise using point estimates, but that, fundamentally, we want to assess and evaluate in its entirety.

As mentioned in Section 5.2.1, this is particularly relevant when there is potential correlation among the model parameters, which we need to reflect appropriately in reporting inference for any function thereof, as is the case in the survival analysis, when we are not just interest in \(\boldsymbol\theta\), as much as we are in \(g(\boldsymbol\theta)=S(t\mid\boldsymbol\theta)\).

Frequentist procedures (such as those used by flexsurv in the background) achieve this through bootstrapping, which, numerically, can be thought of as a (sometimes, but not universally) precise approximation to the full posterior distribution – but again, as the model complexity increases to mimic more closely the complex reality we are trying to understand and estimate, the computational complexity in moving to the Bayesian approach becomes marginally lower and thus potentially much more efficient.

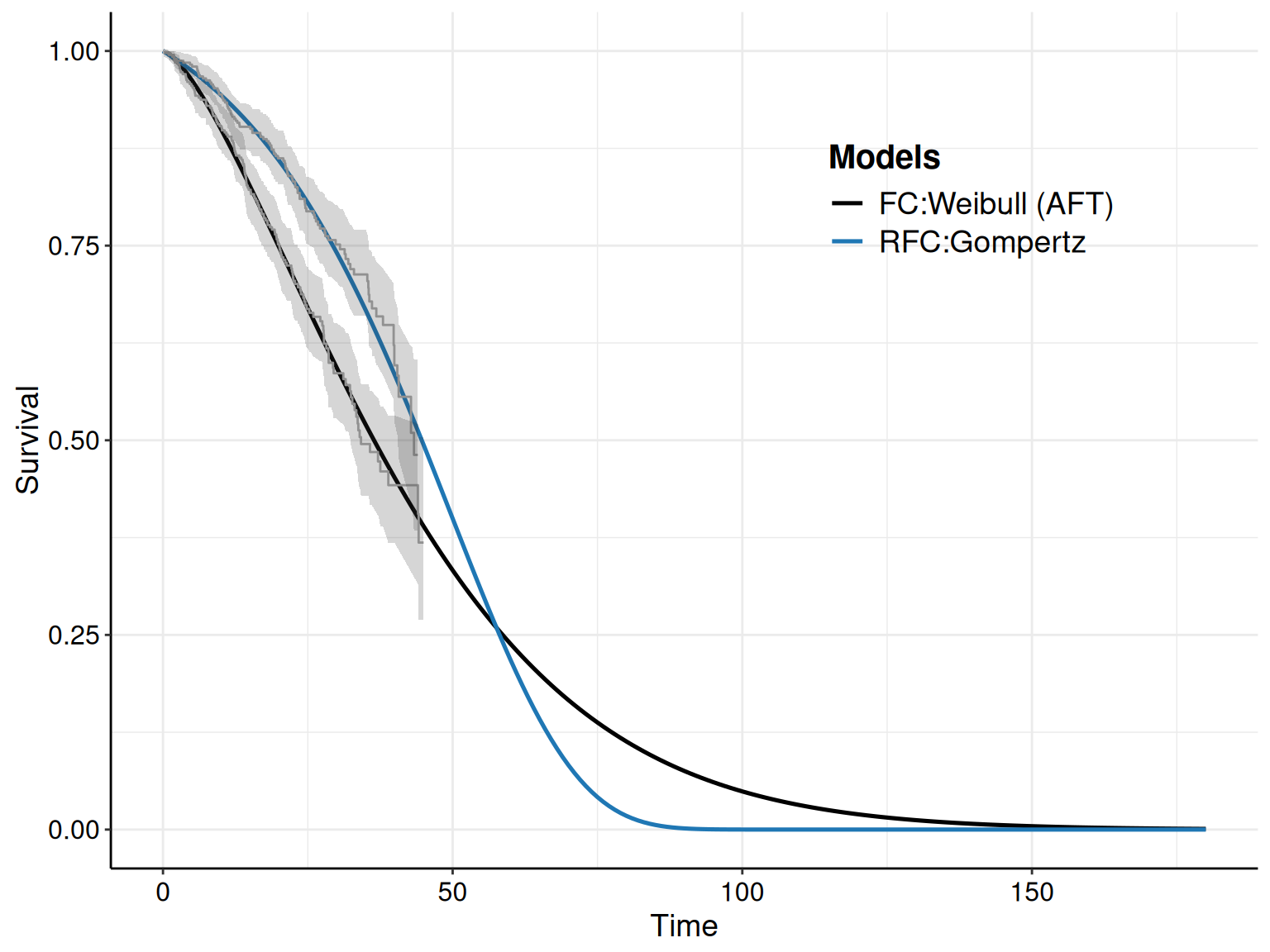

Example 8.7. NICE TA174 (continued): probabilistic sensitivity analysis. The code plot(m,nsim=1000) is sufficient to extend the plot shown in Figure 8.5 and add a 95% interval band around the point estimate for \(S(t\mid\boldsymbol\theta)\).

Looking at multiple survival curves, with the uncertainty around them, within the same plot becomes however quite confusing; for this reason, we can also use the optional argument mods, which allows us to select only one of a few of the distributions fitted in the object m.

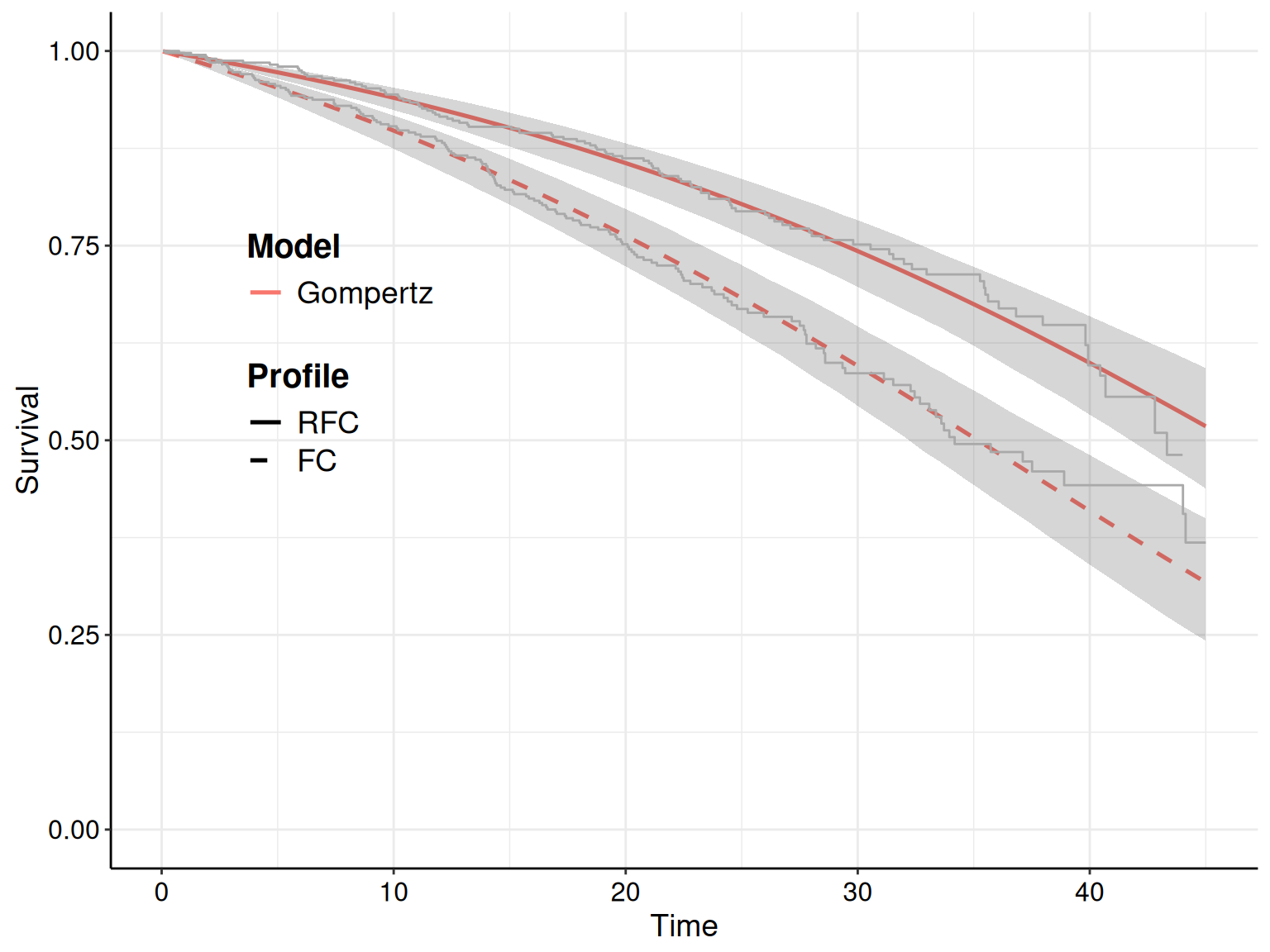

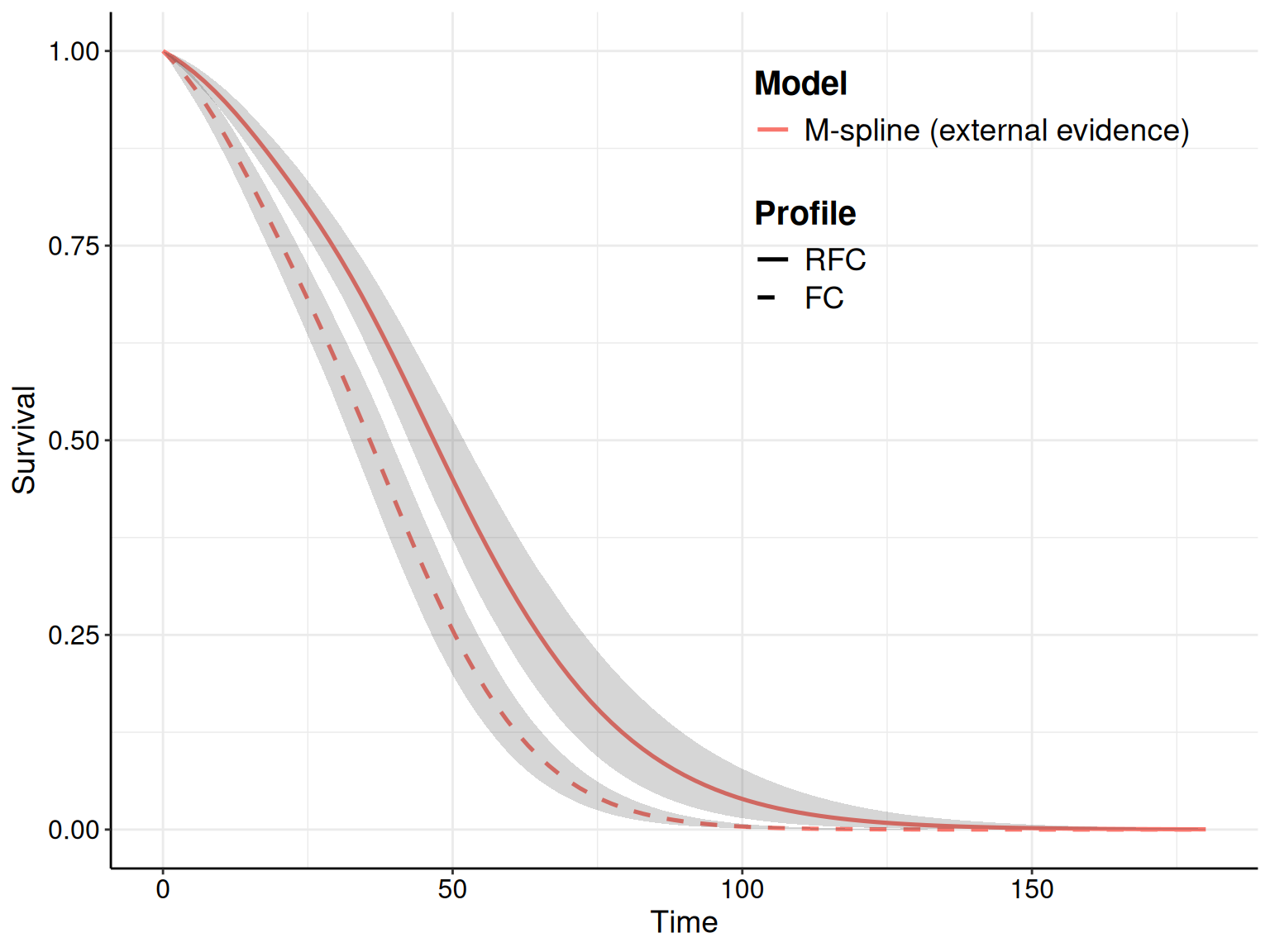

For instance, as we have specified in the call to the function fit.models() the option distr=c("wei","gom","lno") to fit the three distributions in the same object, we can simply use the plot() method with the option mods=2 to instruct R to only show the survival curve for the second model (i.e. the Gompertz), as shown in Figure 8.7.

The R code below takes advantage of the fact that the plot() function in survHE generates a ggplot object and, as such, we can manipulate it for further customisation. First, we save the plot onto an object p – this makes it easier to modify its components. Here we choose to add both the KM estimates (with the interval around the step curve), as well as the point and interval estimates for the survival curve for the Gompertz model.

# Saves the plot to a 'ggplot' object, named p, for further customisation

p=plot(

m,

# Selects only the Gompertz model (the 2nd in the argument 'distr' when

# calling the function fit.models() to obtain the object 'm')

mods=2,

# Adds the KM curves

add.km=TRUE,

# Customises the treatment labels

lab.profile=c("RFC","FC"),

# Uses 'nsim=1000' simulations from the posterior to do the PSA

nsim=1000

)If we just show the resulting plot (by just calling p in the R terminal), we see that the picture is very busy, with multiple uncertainty bands overlaid on top of each other, which makes it very confusing and hard to process. We can still post-process this object to remove the bands around the KM estimate, while including the step function so that we can assess how closely the point and interval around the survival curve matches the KM.

In fact, the newly created object p contains several elements, including one named layers, which describes the features of the various parts that make up the plot. We can visualise what these are using the command p$layers – in this case, there are four parts. A little trial and error (or deeper knowledge of the ggplot machinery…), allows us to identify that the fourth one:

p$layers[[4]]mapping: x = ~time, y = ~S, ymin = ~lower, ymax = ~upper, group =

~as.factor(strata:object_name)

geom_ribbon: na.rm = FALSE, orientation = NA, lineend = butt, linejoin = round,

linemitre = 10, outline.type = both

stat_identity: na.rm = FALSE position_identityis actually the one we want to remove, i.e. the interval bands around the KM estimates. We can do this by setting that layer to NULL and then show the revised object p.

# Removes the 'ggplot' layer showing the interval estimate around the KM curves

p$layers[[4]]=NULL

# Shows the revised plot and customise the position of the legend